How to Improve Cash Flow for Singapore Businesses

Overview

Effective cash flow management in Singapore involves accurate forecasting, accelerating receivables, controlling expenses, and managing inventory to ensure business stability. Regular reviews, timely invoicing, negotiating favorable payment terms, and maintaining a cash reserve help optimize liquidity and reduce vulnerabilities. Using reliable tools and professional bookkeeping supports informed decisions, strengthening financial resilience over time.

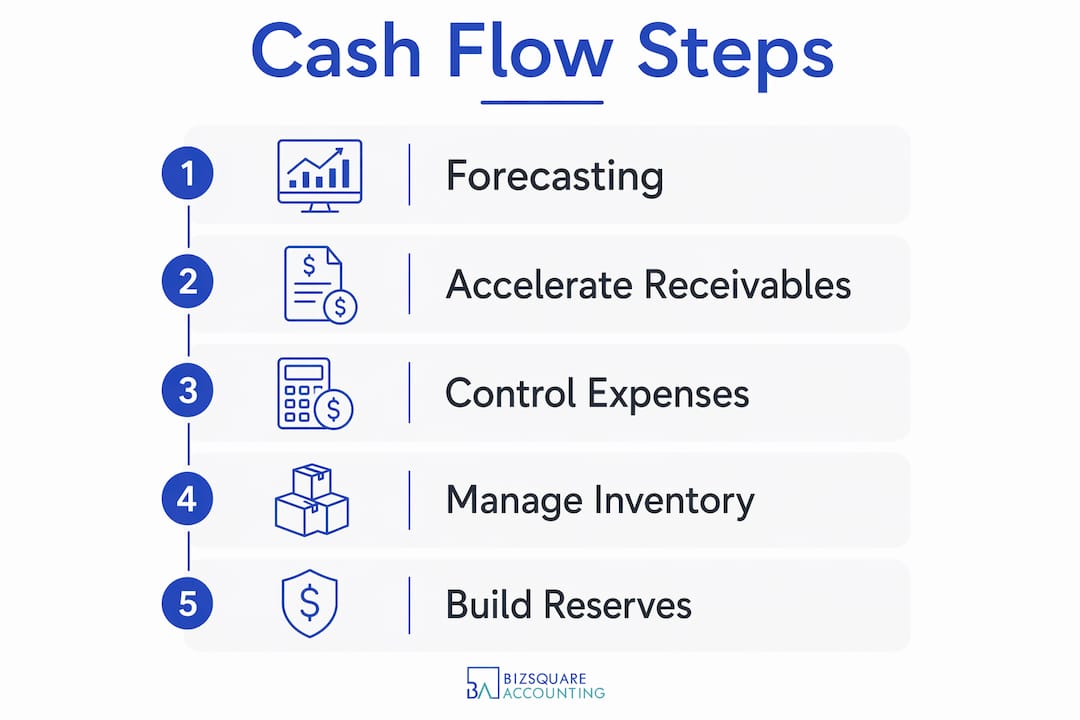

Cash flow improvement is defined as the process of optimizing the timing and volume of money moving into and out of a business to maintain consistent liquidity. For Singapore business owners and financial managers, knowing how to improve cash flow is not optional. It is the difference between a company that survives a slow quarter and one that does not. Tools like FreshBooks, BILL, and cash flow forecasting software give businesses the visibility they need to act before problems arrive, not after. High sales volume does not guarantee positive cash flow without proper accounts receivable, payable, and inventory management in place. The strategies in this article cover every major lever available to Singapore businesses, from forecasting to reserves.

How to improve cash flow through accurate forecasting

Cash flow forecasting is the practice of projecting future cash inflows and outflows over a defined period. It gives business owners the ability to anticipate shortfalls before they become crises. Without a forecast, financial decisions are reactive. With one, they become deliberate.

Small businesses should review cash flow weekly and update their forecasts monthly to avoid critical shortfalls. Weekly reviews catch timing gaps early, while monthly updates align projections with actual business performance. Together, they create a rhythm of financial awareness that most businesses lack.

Two main approaches exist for forecasting: spreadsheets and dedicated software. Spreadsheets like Microsoft Excel or Google Sheets work for early-stage businesses with simple cash flows. Software tools like Xero, QuickBooks, or Float offer automated data pulls, scenario modeling, and real-time dashboards. For Singapore SMEs managing multiple revenue streams, software is the more reliable choice.

Scenario planning is a critical part of forecasting. A business should model at least three scenarios: a base case, a conservative case assuming 20% lower revenue, and a stress case assuming a major client delays payment by 60 days. Each scenario reveals a different set of decisions to prepare for.

Mapping cash flows on a calendar reveals the timing gaps between paying expenses and receiving cash. This calendar view shows exactly which weeks carry the highest outflow risk. Businesses can then schedule financing draws or delay discretionary spending to match their actual cash rhythm.

Pro Tip: Set a recurring calendar reminder every Monday to review last week’s cash position against your forecast. This 15-minute habit prevents most cash surprises.

Key forecasting practices to build into your process:

- Review actual vs. forecast variance every week and document the reasons for gaps.

- Update your 13-week rolling forecast at the start of each month.

- Include tax payment dates, GST filing deadlines, and CPF contribution dates in your cash calendar.

- Model at least one stress scenario per quarter to test your financial resilience.

- Use your forecast to decide when to draw on a credit line, not after the shortfall arrives.

What are the best ways to manage receivables and speed up payments?

Accelerating cash collection is one of the fastest ways to enhance cash flow without taking on debt. The core principle is simple: the faster you invoice, the faster you get paid. Most businesses leave money on the table by delaying invoices or accepting vague payment terms.

Automated invoicing software like FreshBooks and BILL reduces errors and speeds up billing cycles. These tools send invoices immediately after a job is completed, track payment status, and send automated reminders. Manual invoicing, by contrast, introduces delays and human error at every step.

Follow these steps to tighten your receivables process:

- Invoice immediately. Send the invoice the same day a product is delivered or a service is completed. Every day of delay is a day of lost cash.

- Set clear payment terms. State “Net 15” or “Net 30” explicitly on every invoice. Avoid vague language like “payment due upon receipt.”

- Offer early payment discounts. Discounts for early payments motivate faster cash collection. A 2% discount for payment within 10 days is a standard and effective incentive.

- Accept multiple payment methods. Offer PayNow, bank transfer, credit card, and payment portals. Reducing friction in the payment process removes the most common excuse for delays.

- Apply late payment penalties. State your penalty terms clearly on the invoice. Late fees signal that your payment terms are serious, not suggestions.

- Follow up systematically. Send a reminder three days before the due date, on the due date, and three days after. Automate this sequence using your invoicing software.

For businesses with large outstanding invoices, invoice factoring provides an alternative path to liquidity. Invoice factoring advances up to 90% of invoice value upfront and takes over collections from the factoring company. This reduces the cash conversion cycle significantly, which is the time between delivering a product or service and receiving payment.

Pro Tip: For Singapore B2B businesses, consider using an invoicing service that integrates with your accounting system. This eliminates double entry and gives you real-time visibility into outstanding balances.

How do expense control and payables management protect cash flow?

Controlling outflows is just as important as accelerating inflows. Optimizing cash flow involves both defensive measures like expense audits and vendor management, and proactive steps like automated invoicing and payment portals. Most businesses focus only on the proactive side and neglect the defensive work.

An expense audit is the starting point. Review every recurring cost monthly and categorize each as essential, discretionary, or redundant. Redundant costs, such as unused software subscriptions or duplicate vendor contracts, should be cut immediately. Discretionary costs should be reviewed against current revenue levels before renewal.

Payables management is equally important. The goal is to pay on time, not early, unless an early payment discount makes financial sense. Paying early without a discount is a voluntary reduction in your cash position.

Key practices for managing expenses and payables:

- Negotiate longer payment terms with suppliers. Longer vendor payment terms improve cash flow timing by extending the window between receiving goods and paying for them. Ask for Net 45 or Net 60 terms, especially with suppliers you have a long relationship with.

- Prioritize payments by due date and interest rate. Pay obligations with the highest penalties or interest rates first. This minimizes the cost of any temporary cash shortfall.

- Consolidate vendors where possible. Buying from fewer suppliers increases your purchasing volume with each one, which creates leverage for bulk discounts and more flexible terms.

- Require multi-person sign-off for large purchases. This accountability measure prevents impulsive spending and ensures every major outflow is reviewed against the current cash position.

- Reconcile accounts daily. Daily reconciliation catches errors, duplicate charges, and unauthorized transactions before they compound. Xero and QuickBooks both support automated daily bank reconciliation.

Understanding the difference between bookkeeping and accounting helps business owners assign the right tasks to the right people, which reduces errors in payables management.

Does inventory management affect cash flow?

Inventory is one of the most overlooked cash flow levers in product-based businesses. Every dollar tied up in unsold stock is a dollar that cannot pay salaries, cover rent, or fund growth. The relationship between inventory and cash flow is direct and significant.

Overstocking inventory ties up cash and can lead to liquidity shortages. Just-in-time inventory management reduces this risk by ordering stock only when it is needed, based on actual demand signals rather than assumptions. Singapore businesses with limited warehouse space benefit doubly from this approach, since storage costs in Singapore are high.

Technology integration is the practical path to better inventory control. Point-of-sale systems, inventory management platforms like TradeGecko (now QuickBooks Commerce), and ERP systems provide real-time data on stock levels, turnover rates, and reorder points. This data replaces guesswork with precision.

| Inventory Practice | Cash Flow Impact | Recommended Action |

|---|---|---|

| Overstocking | Ties up cash, increases storage costs | Set maximum stock levels based on 30-day sales data |

| Understocking | Causes lost sales and emergency orders | Set reorder points with automatic purchase triggers |

| Obsolete stock | Locks up capital with no return | Review and liquidate slow-moving items quarterly |

| Just-in-time ordering | Frees cash, reduces storage costs | Align order cycles with confirmed sales or contracts |

Reviewing and liquidating obsolete stock is a discipline many businesses avoid because it means accepting a loss. The reality is that holding obsolete stock costs money every month through storage, insurance, and opportunity cost. Selling it at a discount recovers partial value and frees cash immediately.

Pro Tip: Run a quarterly stock age report in your inventory system. Any item that has not moved in 90 days should be flagged for a liquidation decision. Waiting longer rarely improves the outcome.

Process improvements also reduce cash consumption. Reviewing procurement workflows, eliminating redundant approval steps, and standardizing order quantities all reduce the administrative cost of managing inventory. Leaner operations translate directly into better cash positions.

Should you build cash reserves or rely on credit lines?

Cash reserves and credit lines serve different purposes, and the strongest businesses maintain both. Reserves provide a buffer against unexpected shortfalls. Credit lines provide flexibility for growth opportunities or timing mismatches. Relying on only one of these creates unnecessary vulnerability.

A cash reserve equivalent to three months of operating expenses is the recommended minimum for small businesses. This cushion covers payroll, rent, and supplier payments during a slow period or a major client delay. Building this reserve takes time, but the process is straightforward: set aside a fixed percentage of monthly revenue into a dedicated account until the target is reached.

Automatic savings methods remove the temptation to spend reserve funds. Setting up a standing instruction to transfer a fixed amount to a separate savings account each month makes reserve building a non-negotiable process. Singapore businesses can use OCBC, DBS, or UOB business savings accounts for this purpose.

| Option | Best Use Case | Key Consideration |

|---|---|---|

| Cash reserve | Emergency coverage, short-term shortfalls | Target 3 months of operating expenses |

| Business credit line | Bridging payment timing gaps | Use strategically, repay quickly to minimize interest |

| Business credit card | Small recurring expenses, vendor payments | Pay in full monthly to avoid interest charges |

| Equipment leasing | Preserving cash for operations | Leasing avoids large upfront capital outflows |

| Invoice factoring | Immediate liquidity from outstanding invoices | Factor only when the cost is justified by the cash need |

Leasing equipment instead of buying it outright preserves cash for operations. A business that spends $50,000 on a piece of equipment depletes its reserve immediately. The same business that leases the equipment for $1,500 per month keeps its cash available for payroll and growth. For Singapore businesses managing tight cash positions, leasing is often the more practical choice.

Successful cash flow management means shifting from reactive fixes to a predictable cash rhythm. Credit lines should be drawn based on a forecast, not in response to a crisis. Businesses that use credit proactively, drawing before a known shortfall and repaying as receivables come in, pay less interest and maintain better lender relationships.

Understanding cash flow management in business at a structural level helps owners make better decisions about when to use reserves versus credit.

Key takeaways

Improving cash flow requires a combination of forecasting discipline, receivables acceleration, expense control, inventory efficiency, and reserve building, applied consistently over time.

| Point | Details |

|---|---|

| Forecast weekly and monthly | Review cash position every week and update your rolling forecast monthly to catch shortfalls early. |

| Automate invoicing immediately | Use tools like FreshBooks or BILL to send invoices the same day work is completed and reduce collection delays. |

| Negotiate vendor payment terms | Request Net 45 or Net 60 terms with suppliers to extend your payable window and preserve cash. |

| Maintain a three-month reserve | Keep at least three months of operating expenses in a dedicated account as a financial cushion. |

| Liquidate obsolete inventory quarterly | Review slow-moving stock every 90 days and sell it at a discount to recover cash tied up in unsold goods. |

Cash flow realities singapore business owners often miss

Most cash flow problems I see in Singapore businesses are not caused by low revenue. They are caused by poor timing. A business can have strong sales in January and still miss payroll in February because clients pay on Net 60 terms and suppliers demand payment in 30 days. That timing gap is the real enemy.

The businesses that manage cash flow well share one habit: they treat their cash forecast as a live document, not a quarterly exercise. They update it when a major client delays payment. They update it when a new contract is signed. They treat it the way a pilot treats an instrument panel, checking it constantly, not just when something feels wrong.

Another pattern I observe is that business owners in Singapore tend to be reluctant to negotiate payment terms. They fear losing a client or a supplier relationship. The reality is that most suppliers expect negotiation. Asking for Net 45 instead of Net 30 is a normal business conversation. The businesses that ask get better terms. The ones that do not ask pay the price in cash shortfalls.

The combination of professional bookkeeping services and a clear cash flow forecast is the most reliable foundation for financial stability. Bookkeeping keeps your numbers accurate. The forecast tells you what those numbers mean for the next 90 days. Without both, you are managing by instinct, and instinct is not a cash flow strategy.

How Bizsquare helps singapore businesses manage cash flow

Bizsquare provides the financial infrastructure that makes cash flow improvement practical, not theoretical. From accurate bookkeeping to corporate advisory and tax planning, Bizsquare’s services give Singapore business owners the data and guidance they need to make confident financial decisions.

Bizsquare’s accounting and bookkeeping services maintain real-time financial records that feed directly into cash flow forecasting. The corporate advisory and outsourced CFO services provide strategic guidance on payment terms, reserve building, and credit management. For businesses starting out, Bizsquare’s company incorporation services set up the right financial structure from day one. Contact Bizsquare today to build a cash flow management system that works for your business.

FAQ

1) What is the fastest way to improve cash flow?

The fastest way to improve cash flow is to accelerate receivables collection. Send invoices immediately after completing work, offer early payment discounts, and follow up on overdue accounts within three days of the due date.

2) How often should a business review its cash flow forecast?

Small businesses should review their cash flow weekly and update their full forecast monthly. Weekly reviews catch timing problems early, while monthly updates align projections with actual business performance.

3) What is invoice factoring and how does it help cash flow?

Invoice factoring is the sale of unpaid invoices to a third party in exchange for immediate cash. It advances up to 90% of invoice value upfront, reducing the time between delivering a service and receiving payment.

4) How much cash reserve should a singapore business maintain?

A cash reserve equivalent to at least three months of operating expenses is the recommended minimum. This covers payroll, rent, and supplier payments during slow periods or unexpected disruptions.

5) What is the difference between cash flow and profit?

Profit is the difference between revenue and expenses on paper. Cash flow is the actual movement of money in and out of the business. A profitable business can still face a cash crisis if its receivables are slow and its payables are fast.

6) How does inventory management affect cash flow?

Overstocking ties up cash in unsold goods, while understocking leads to emergency orders at higher costs. Just-in-time inventory management aligns stock levels with actual demand, freeing cash for operations.

7) What payment terms should singapore businesses offer customers?

Net 15 or Net 30 terms are standard for Singapore B2B transactions. Offering a 2% discount for payment within 10 days is an effective incentive for faster collection without significantly reducing margins.

8) Can a business improve cash flow without cutting costs?

Yes. Accelerating receivables, negotiating longer payable terms, and improving inventory turnover all improve cash flow without reducing expenses. Cost cutting is one tool, not the only one.

9) What tools help with cash flow management in singapore?

Xero, QuickBooks, and Float are widely used for cash flow forecasting in Singapore. FreshBooks and BILL automate invoicing and payment tracking. These tools integrate with Singapore bank accounts and support GST reporting.

10) When should a business use a credit line instead of its cash reserve?

Use a credit line to bridge known, short-term timing gaps between payables and receivables. Reserve the cash reserve for genuine emergencies or unexpected shortfalls. Drawing on credit proactively, based on a forecast, reduces interest costs compared to emergency draws.

11) How does professional bookkeeping improve cash flow accuracy?

Accurate bookkeeping ensures that every transaction is recorded correctly and on time. This accuracy feeds into reliable cash flow forecasts, which prevents decisions based on incorrect financial data.

12) What is a cash flow management checklist for singapore smes?

A practical cash flow management checklist includes weekly cash reviews, monthly forecast updates, immediate invoicing, vendor term negotiations, quarterly inventory audits, and maintaining a three-month operating expense reserve.

13) How does GST affect cash flow for singapore businesses?

GST-registered businesses in Singapore collect GST from customers but must remit it to IRAS quarterly. This creates a timing gap where collected GST sits in the business account temporarily. Planning for GST payment dates in your cash calendar prevents shortfalls at filing time.