Corporate Tax Service in Singapore: 2026 Guide

Overview

A corporate tax service offers specialized assistance to help businesses comply with IRAS, reduce liabilities, and maximize benefits. In 2026, accurate filings are critical to claim automatic rebates and grants, making expert guidance essential for optimal savings. Using technology and proactive advice, professional firms enable companies to effectively navigate tax incentives and avoid costly errors.

A corporate tax service is defined as specialized professional assistance that helps businesses meet tax obligations, reduce liabilities, and stay compliant with the Inland Revenue Authority of Singapore (IRAS). For Singapore business owners in 2026, this support carries extra weight. The government has introduced a 40% corporate tax rebate capped at S$30,000, plus a S$2,000 cash grant for active companies employing at least one local worker in 2025. IRAS applies these benefits automatically, but only businesses with accurate, timely filings actually receive them. That is where qualified corporate tax advisors, like those at Bizsquare, make the difference between leaving money on the table and capturing every dollar available.

What does a corporate tax service include?

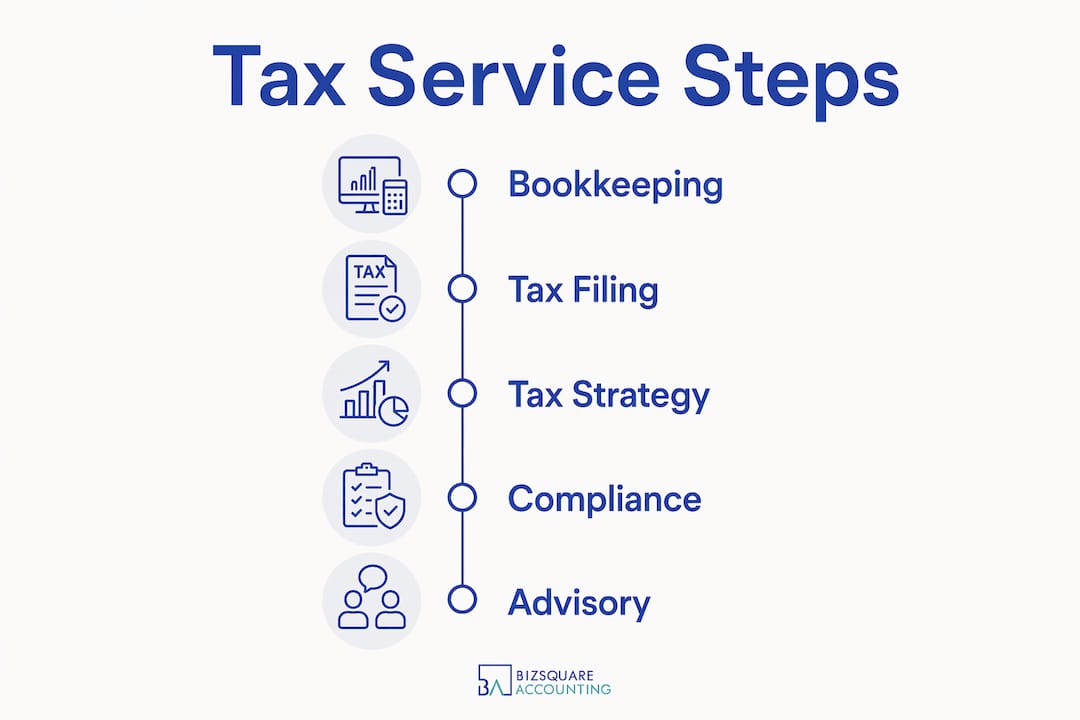

Corporate tax services span a wide range, from basic return filing to full strategic tax advisory. Understanding what is typically included helps business owners choose the right level of support for their needs.

The core components of a professional corporate tax service are:

- Tax compliance and filing: Preparing and submitting corporate tax returns to IRAS on time, including Form C-S or Form C depending on company size and structure.

- Tax planning: Identifying legal deductions, rebates, and exemptions to reduce the overall tax bill before the assessment year closes.

- Business tax consulting: Providing strategic advice on structuring transactions, managing cross-border activities, and responding to regulatory changes.

- Audit support: Representing the company during IRAS queries or audits, preparing documentation, and managing correspondence.

- Technology integration: Using cloud-based accounting software and tax tools to maintain accurate records that feed directly into tax filings.

- Bookkeeping coordination: Aligning financial records with tax reporting requirements so that no deductible expense is missed.

Each of these components connects to the others. A company with clean bookkeeping files faster and more accurately. A company with a clear tax plan captures more deductions. The most effective corporate tax service providers treat these functions as one integrated system, not separate tasks.

Pro Tip: Ask any prospective tax firm whether their bookkeeping and tax teams share the same client file. Firms that separate these functions often miss deductions that sit in the accounting records.

Tax strategy consulting is the component most businesses underuse. Many owners treat tax as a year-end task rather than a year-round discipline. A qualified tax advisor reviews the business structure, planned capital expenditures, and hiring decisions throughout the year. This forward-looking approach consistently produces better outcomes than reactive filing alone.

How do corporate tax services optimize liabilities in 2026?

Singapore’s 2026 tax incentives create real, measurable savings for businesses that claim them correctly. The key is knowing exactly what is available and how each benefit applies to your company.

2026 corporate tax incentives at a glance

| Incentive | Eligibility | Benefit |

|---|---|---|

| Corporate Tax Rebate | Active companies with at least 1 local employee in 2025 | 40% rebate on tax payable, capped at S$30,000 |

| Cash Grant | Same eligibility as above | S$2,000 cash grant per qualifying company |

| Market Readiness Assistance (MRA) | SMEs expanding internationally | Up to 70% grant support; deduction cap raised from S$150,000 to S$400,000 |

| Non-SME International Expansion | Non-SMEs with qualifying overseas expenses | 50% grant support under the MRA scheme |

The 40% rebate is significant for profitable companies. A business with S$75,000 in tax payable, for example, would receive a S$30,000 reduction, bringing the effective liability down to S$45,000. That is not a minor adjustment. It is a material cash flow benefit that directly affects working capital.

IRAS processes these rebates through automated disbursement in Q2 2026. No manual application is required. This removes administrative burden, but it also means the accuracy of your filed return determines the rebate amount. Errors in the return translate directly into a smaller rebate.

Corporate tax advisors add value here in two specific ways. First, they verify that all qualifying local employment records are documented correctly before filing. Second, they review whether the company qualifies for the MRA scheme, which raises the tax deduction cap for internationalization expenses from S$150,000 to S$400,000. For companies with overseas marketing, trade fair participation, or market entry costs, this enhancement is substantial.

Pro Tip: If your company incurred any overseas business development expenses in 2025, ask your tax advisor to assess MRA eligibility before filing. Many SMEs qualify but never claim because the scheme is not well publicized.

Tax saving strategies for Singapore businesses extend beyond rebates. Proper capital allowance claims, writing-down allowances on intellectual property, and deductions for research and development expenditure all reduce taxable income. A skilled tax advisor reviews each of these categories systematically, not just the obvious ones.

DIY, in-house, or professional firm: which tax service fits your business?

Business owners in Singapore generally choose from three approaches to corporate tax management. Each has a different cost profile, risk level, and capability ceiling.

Comparing your options

| Approach | Best For | Key Advantage | Key Limitation |

|---|---|---|---|

| DIY with software | Dormant or very simple companies | Lowest upfront cost | High error risk, misses deductions |

| In-house accountant | Mid-size firms with routine tax needs | Direct access, business familiarity | Limited specialist tax knowledge |

| Professional tax firm | Growing SMEs, complex structures, international activity | Deep expertise, audit defense, full optimization | Higher fee, requires good record-keeping |

DIY filing using basic accounting software works for dormant companies or sole proprietors with minimal transactions. For active companies with employees, multiple revenue streams, or any cross-border activity, DIY approaches carry real risk. Professional corporate tax preparation costs more upfront but consistently produces better financial outcomes by preventing costly errors and penalties.

In-house accountants provide continuity and business context. They know the company’s operations well. However, tax law in Singapore changes regularly, and most in-house accountants do not specialize in corporate tax advisory. They handle bookkeeping and basic compliance competently, but they rarely provide the proactive planning that reduces tax liabilities year over year.

Professional corporate tax firms offer the highest level of capability. Tailored tax strategies from experienced advisors minimize risks and maximize savings using advanced tools and direct access to senior tax partners. This matters most when a company faces an IRAS query, has complex related-party transactions, or is expanding into new markets.

The decision to outsource tax work often comes down to one question: what is the cost of getting it wrong? For a company with S$500,000 in annual revenue, a missed deduction or a late filing penalty can easily exceed the annual fee of a professional firm. The math favors professional support in most active business scenarios.

When evaluating firms, look for these qualities:

- Demonstrated experience with IRAS filings and audit representation

- Clear communication on fees and scope of work

- Integration with your existing accounting or bookkeeping setup

- Proactive updates on regulatory changes, not just year-end contact

Step-by-step: corporate tax compliance in singapore for 2026

Corporate tax compliance requires meeting annual deadlines set by IRAS and preparing accurate documentation. Missing these steps can result in fines and additional scrutiny. Follow this process to stay on track.

- Close your financial year accounts. Singapore companies typically have a December 31 financial year-end, though other dates are permitted. Finalize all revenue, expense, and balance sheet entries before proceeding.

- Prepare your tax computation. Calculate taxable income by adjusting accounting profit for non-deductible expenses, capital allowances, and applicable deductions. This step requires knowledge of the Income Tax Act.

- Coordinate with your tax advisor or firm. Share finalized accounts, payroll records, and any supporting documents for deduction claims. Your advisor reviews the computation and identifies any missed opportunities.

- File the Estimated Chargeable Income (ECI). Companies must file ECI with IRAS within three months of the financial year-end. For a December 31 year-end, this means filing by March 31.

- Submit the annual corporate tax return. File Form C-S (for companies with revenue below S$5 million and meeting other criteria) or Form C by November 30 of the assessment year. Accuracy here determines your rebate amount under the 2026 scheme.

- Monitor IRAS correspondence and rebate disbursement. IRAS processes the 40% rebate and S$2,000 cash grant automatically in Q2 2026. Confirm receipt and reconcile against your tax computation.

- Address any IRAS queries promptly. If IRAS raises questions about your return, respond within the stated deadline. Your tax advisor should manage this process on your behalf.

- Review and plan for the next year. After filing, conduct a post-assessment review with your advisor. Identify structural changes, planned investments, or hiring decisions that affect next year’s tax position.

Late filings result in penalties under the Income Tax Act. IRAS may impose fines and, in repeated cases, pursue legal action. The best way to avoid penalties is to build a filing calendar at the start of each year and assign clear responsibility for each step.

How is technology changing corporate tax services?

AI, cloud solutions, and data analytics are reshaping how corporate tax services are delivered in Singapore. These tools improve accuracy, reduce manual work, and help businesses respond to regulatory changes faster.

Key developments include:

- AI-powered tax review: Automated tools scan financial records for deduction opportunities and flag inconsistencies before filing. This reduces human error and speeds up the review process.

- Cloud-based accounting integration: Platforms like Xero and QuickBooks connect directly with tax preparation workflows. Real-time data means tax advisors work from current figures, not month-old exports.

- Data analytics for tax planning: Advanced firms use analytics to model different tax scenarios, comparing the impact of capital expenditure timing, entity restructuring, or new hiring on the overall tax position.

- Real-time compliance monitoring: Regulatory update tools alert advisors and clients when IRAS changes filing requirements or introduces new incentives. This is particularly valuable given the pace of Singapore’s Budget announcements.

- Digital document management: Secure cloud storage for invoices, contracts, and payroll records makes audit defense faster and more organized.

SMEs benefit from these tools as much as large enterprises. A small company using a cloud-based bookkeeping service that integrates with its tax advisor’s platform effectively operates with the same data infrastructure as a much larger firm. The cost of these tools has dropped significantly, making professional-grade tax management accessible at every business size.

The practical implication for business owners is straightforward. Choosing a tax service provider that uses current technology is not optional. Firms still relying on manual spreadsheets and email-based document transfers introduce unnecessary risk into the compliance process.

Key takeaways

Effective corporate tax management in Singapore requires accurate filings, proactive planning, and the right professional support to capture every available incentive.

| Point | Details |

|---|---|

| 2026 rebate is automatic | IRAS applies the 40% rebate and S$2,000 grant without manual application, but only if filings are accurate. |

| Professional firms outperform DIY | Outsourcing to qualified tax advisors prevents errors, captures deductions, and provides audit defense. |

| MRA scheme raises deduction caps | SMEs expanding internationally can claim up to S$400,000 in qualifying expenses under the 2026 MRA enhancement. |

| Technology improves outcomes | Tax firms using AI, cloud tools, and analytics deliver faster, more accurate filings than manual processes. |

| Compliance is year-round | ECI filing, annual returns, and proactive planning require attention throughout the year, not just at year-end. |

Why most businesses underestimate their tax position

The most common mistake I see among Singapore business owners is treating corporate tax as a compliance checkbox rather than a financial management tool. Filing on time matters, but it is the floor, not the ceiling.

The 2026 Budget incentives illustrate this clearly. The 40% rebate and the MRA deduction cap increase are genuinely significant. Yet many businesses will receive a smaller benefit than they are entitled to, simply because their records are incomplete or their advisor did not review MRA eligibility. That is not a regulatory failure. It is a planning failure.

The warning signs of an inadequate tax service provider are consistent. They contact you only at year-end. They ask you to prepare your own tax computation. They cannot explain the basis for each deduction claim. They have no process for tracking regulatory updates between Budget announcements. These are not minor service gaps. They represent real financial risk.

Proactive tax strategy consulting changes the outcome. A good advisor reviews your business structure, your hiring plans, and your capital expenditure schedule before the financial year closes. They identify whether restructuring a transaction or accelerating a purchase changes your tax position materially. This kind of forward-looking work is what separates a tax compliance service from a genuine tax advisory relationship.

For growing companies, the value of expert advisory compounds over time. Each year of proactive planning builds a cleaner, more defensible tax position. Each year of reactive filing creates accumulated risk. The choice between these two paths is made not at year-end, but when you select your tax service provider.

Work with Bizsquare for trusted corporate tax support

Bizsquare provides corporate tax filing and advisory services built specifically for Singapore businesses. From ECI submissions to full tax strategy reviews, the team at Bizsquare handles every stage of the compliance process with precision and regulatory accuracy.

Bizsquare’s corporate tax advisors stay current with every IRAS update, including the 2026 rebate scheme and MRA enhancements. The firm integrates accounting and bookkeeping services directly with tax preparation, so nothing falls through the gaps. Business owners looking to incorporate and build a compliant tax structure from day one can also explore company incorporation in Singapore through Bizsquare. Contact Bizsquare today to discuss a tax plan tailored to your business size, structure, and growth objectives.

FAQ

1.) What is a corporate tax service?

A corporate tax service is professional assistance that manages a company’s tax filings, planning, and compliance with IRAS requirements. It covers everything from annual return preparation to strategic tax advisory.

2.) Who qualifies for the 2026 Singapore corporate tax rebate?

Active companies that employed at least one local worker in 2025 qualify for a 40% tax rebate capped at S$30,000 and a S$2,000 cash grant. IRAS applies these automatically based on filed returns.

3.) When must Singapore companies file their corporate tax returns?

Companies must file ECI within three months of their financial year-end and submit Form C-S or Form C by November 30 of the assessment year. Late filings result in penalties under the Income Tax Act.

4.) Is it worth hiring a professional firm for corporate tax filing?

Professional corporate tax preparation costs more upfront but prevents errors, captures missed deductions, and provides audit defense. The financial outcome typically exceeds the cost of the service for any active company.

5.) What is the market readiness assistance scheme?

The Market Readiness Assistance (MRA) scheme supports Singapore companies expanding internationally. In 2026, the deduction cap increased from S$150,000 to S$400,000, with SMEs receiving up to 70% grant support on qualifying expenses.

6.) What documents are needed for corporate tax filing in singapore?

Companies need finalized financial statements, payroll records, invoices supporting deduction claims, and a tax computation reconciling accounting profit to taxable income. A tax advisor can prepare or review all of these.

7.) Can a small business use a corporate tax service?

Yes. Small businesses benefit from professional tax services because the cost of errors and missed deductions often exceeds the service fee. Many firms offer tiered pricing suited to SME budgets.

8.) How does IRAS disburse the 2026 tax rebate?

IRAS processes the rebate and cash grant automatically in Q2 2026 based on the company’s filed return. No separate application is required, but the rebate amount depends entirely on the accuracy of the filing.

9.) What is the difference between tax compliance and tax planning?

Tax compliance means meeting filing deadlines and reporting income correctly. Tax planning means structuring business decisions throughout the year to legally reduce the tax liability before the assessment period closes.

10.) How do i know if my current tax service provider is adequate?

A reliable provider contacts you proactively throughout the year, explains each deduction claim clearly, stays current with IRAS updates, and integrates with your bookkeeping records. Year-end-only contact is a clear sign of insufficient service.

11.) What happens if a company files its corporate tax return late in Singapore?

IRAS imposes financial penalties for late filings, and repeated non-compliance can lead to legal action. Filing on time, with accurate documentation, is the most direct way to avoid these consequences.