Why Maintain Proper Financial Records for Your Business

Overview

– Maintaining proper financial records is essential for compliance, tax accuracy, and informed decision-making in Singapore businesses.

– Consistent documentation with completeness, accuracy, and traceability safeguards against penalties and supports business growth.

Proper financial records are the foundation of every compliant, profitable, and well-managed business in Singapore. The term “financial recordkeeping” refers to the systematic practice of capturing, organizing, and retaining all financial transactions, documents, and reports that reflect a company’s economic activity. For Singapore business owners, this practice connects directly to tax compliance under the Inland Revenue Authority of Singapore (IRAS), corporate governance obligations under the Accounting and Corporate Regulatory Authority (ACRA), and the day-to-day decisions that determine whether a business grows or stalls. This guide explains why maintain proper financial records matters, what good documentation looks like, and how to build a system that protects your business.

Why maintaining proper financial records reduces tax risks

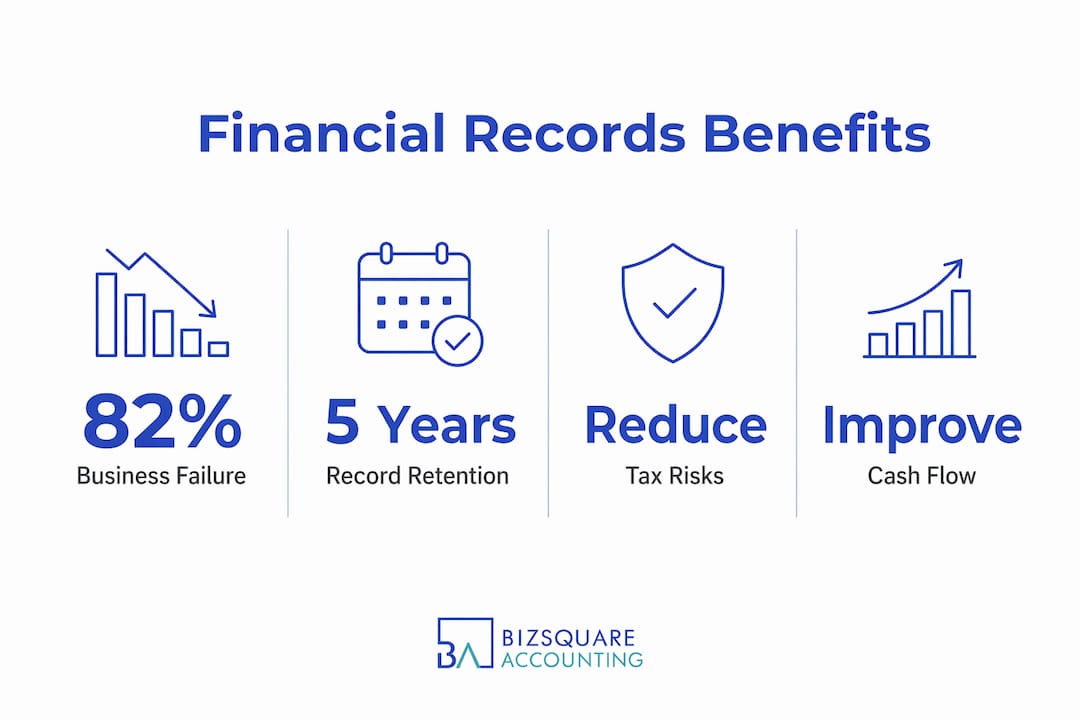

Every Singapore business has a legal obligation to keep financial records that prove its income and deductions. IRAS requires companies to retain source documents, accounting records, and bank statements for a minimum of five years after the relevant Year of Assessment. However, CPA experts recommend retaining financial records for seven years to cover statutes of limitations in disputes or extended audits. That extra buffer matters more than most business owners realize.

When records are incomplete or disorganized, the consequences extend well beyond inconvenience. IRAS auditors can disallow deductions that lack supporting documentation. Penalties, surcharges, and back taxes can accumulate quickly. In serious cases, inadequate recordkeeping can trigger a full audit, which consumes management time and legal fees far exceeding the cost of proper bookkeeping.

Organized records simplify tax filing significantly. When invoices, receipts, payroll records, and bank statements are filed consistently, your accountant or tax agent can prepare accurate returns faster and with fewer queries. This reduces the risk of errors, late submissions, and the penalties that follow.

Key documents to retain for tax compliance include:

- Sales invoices and receipts issued to customers

- Purchase invoices and supplier receipts for all business expenses

- Bank statements reconciled monthly against your accounts

- Payroll records including CPF contribution histories

- Contracts and agreements supporting significant transactions

- GST records if your business is GST-registered

Pro Tip: Set a calendar reminder at the end of each quarter to audit your document folders. Catching gaps early is far less painful than reconstructing records during a tax review.

How financial records support cash flow and business health

Cash flow mismanagement accounts for approximately 82% of small business failures, and poor financial documentation is a primary driver of that mismanagement. This statistic means that most businesses do not fail because their product is bad. They fail because their owners cannot see clearly where money is coming from and where it is going.

Accurate financial records give business owners a real-time picture of their cash position. They reveal which customers pay late, which expenses are growing faster than revenue, and which product lines are actually profitable. Without this visibility, decisions get made on gut feeling rather than evidence.

Consider how financial clarity improves specific business decisions:

- Credit and financing applications. Banks and lenders in Singapore require audited or reviewed financial statements before approving loans. Clean records accelerate approvals and often secure better terms.

- Pricing decisions. Knowing your true cost of goods sold and overhead allocation allows you to price products and services accurately, not just competitively.

- Hiring decisions. Payroll is typically the largest expense for service businesses. Records showing revenue trends help owners decide when hiring is sustainable.

- Vendor negotiations. Tracking payment histories and purchase volumes gives you data to negotiate better terms with suppliers.

- Exit and succession planning. Buyers and investors in Singapore conduct due diligence. Clean, traceable records increase business valuation and reduce deal friction.

Good bookkeeping transforms raw data into actionable intelligence, enabling data-driven decisions and business growth. This means founders who invest in proper recordkeeping are not just staying compliant. They are building a management tool that compounds in value over time.

The importance of bookkeeping services for Singapore businesses goes beyond tax season. Monthly management accounts derived from clean records allow owners to spot trends, manage working capital, and plan for growth with confidence.

What constitutes proper financial documentation

Documentation must ensure completeness, consistency, and traceability for credibility and audit readiness. These three criteria are the standard against which every document set is judged, by auditors, tax authorities, and potential investors alike.

Completeness means every transaction has a full supporting document trail. A complete documentary chain includes purchase orders, invoices, delivery receipts, approvals, and payment confirmations. A single missing link, such as a delivery receipt without a corresponding invoice, creates a gap that auditors will question.

Consistency means documents do not contradict each other. The amount on a purchase order must match the invoice, which must match the payment record. Discrepancies, even minor ones, raise red flags during reviews and can lead to disallowed deductions or extended audit timelines.

Traceability means a third party, such as an IRAS auditor or external accountant, can follow the paper trail from a transaction’s origin to its final recording in your accounts without needing to ask you for explanations. A clear, consistent, and well-organized financial trail builds transparency and management confidence.

The table below compares documentation that meets these criteria against documentation that falls short:

| Criteria | Strong documentation | Weak documentation |

|---|---|---|

| Completeness | Invoice + delivery receipt + payment confirmation present | Invoice only, no proof of delivery or payment |

| Consistency | Purchase order amount matches invoice and bank debit | Invoice amount differs from bank statement entry |

| Traceability | Digital folder with named files and audit trail | Loose paper receipts with no filing system |

| Retention | Stored securely for 5 to 7 years with backups | Stored on a single device with no backup |

Pro Tip: Name digital files using a consistent format such as “YYYY-MM-DD_VendorName_InvoiceNumber” so any team member or auditor can locate a document in seconds.

How to implement effective recordkeeping systems in Singapore

Building a reliable recordkeeping system does not require a large team or expensive technology. It requires discipline, the right tools, and a process that your business follows consistently. The following steps provide a practical framework for Singapore business owners.

- Choose dedicated accounting software. Tools like Xero, QuickBooks, or MYOB are widely used by Singapore SMEs and integrate with local bank feeds, CPF reporting, and GST filing. Manual spreadsheets are error-prone and difficult to audit. Software creates an automatic audit trail.

- Separate business and personal finances immediately. Mixing personal and business finances complicates recordkeeping and can lead to denied deductions and increased audit attention. Open a dedicated business bank account and use it exclusively for company transactions.

- Centralize document storage with access controls. Use cloud storage platforms such as Google Drive or Microsoft SharePoint to store financial documents. Apply folder structures by year and document type. Restrict editing access to authorized personnel only.

- Implement a retention policy aligned with IRAS requirements. IRAS requires a minimum five-year retention period for business records. Set a formal policy that defines what gets kept, where it is stored, and when it can be deleted. Document this policy in writing.

- Reconcile bank statements weekly. Regular weekly reconciliation prevents errors, detects fraud early, and maintains an accurate financial picture. Monthly reconciliation is the minimum acceptable standard, but weekly reviews catch problems before they compound.

- Engage professional support when needed. For SMEs without a full-time finance team, outsourced bookkeeping or an outsourced CFO provides expertise without the overhead of a permanent hire.

Bookkeeping accuracy tips for Singapore SMEs cover practical steps for maintaining reliable records at every stage of business growth. Reviewing these practices periodically helps owners identify gaps before they become compliance issues.

Effective financial document management requires centralization, version control, clear naming conventions, and access controls. Businesses that implement these four elements reduce retrieval time, minimize errors, and demonstrate audit readiness at any point in the year.

Pro Tip: Schedule a monthly “finance hour” where you or your bookkeeper reviews outstanding invoices, reconciles accounts, and files any documents received during the month. Consistency over time eliminates year-end scrambles.

Common mistakes in financial recordkeeping and how to avoid them

Many Singapore business owners understand the importance of financial documentation in theory but fall into predictable patterns that undermine their records in practice. Recognizing these mistakes is the first step toward correcting them.

- Mixing personal and business accounts. This is the most common and most damaging error. It makes it impossible to determine true business profitability and creates immediate red flags for IRAS auditors. The fix is simple: open a separate business account on day one of operations.

- Keeping incomplete documentation. Retaining an invoice but discarding the delivery receipt or payment confirmation breaks the documentary chain. Every transaction needs its full set of supporting documents, not just the primary invoice.

- Delaying reconciliation. Many owners reconcile accounts quarterly or only at year-end. By then, errors have compounded, missing documents are harder to retrieve, and discrepancies take longer to resolve. Weekly or at minimum monthly reconciliation is the correct practice.

- Ignoring legal retention requirements. ACRA and IRAS both specify retention periods for different document types. Deleting records before the required period expires exposes the business to penalties and leaves it defenseless in an audit.

- Failing to back up digital records. Storing financial records on a single laptop or local hard drive creates a single point of failure. A hardware failure or ransomware attack can destroy years of records. Cloud backups with version control are non-negotiable.

- Relying on memory instead of documentation. Without proper documentation, transactions, even real ones, may not be accepted during audits or legal disputes. The principle in accounting is clear: what is not documented is difficult to defend.

The impact of poor financial records on Singapore businesses ranges from disallowed tax deductions to failed financing applications and, in the worst cases, regulatory penalties from ACRA or IRAS. Prevention is always less costly than remediation.

Key takeaways

Proper financial recordkeeping is both a legal requirement and a strategic asset for every Singapore business, protecting against tax penalties while enabling smarter, evidence-based decisions.

| Point | Details |

|---|---|

| Legal retention requirement | IRAS requires records for at least five years; seven years is the recommended standard for full protection. |

| Cash flow visibility | Accurate records prevent the cash flow mismanagement linked to 82% of small business failures. |

| Documentation quality | Every transaction needs completeness, consistency, and traceability to withstand audit scrutiny. |

| System implementation | Dedicated accounting software, separated accounts, and weekly reconciliation form the core of a reliable system. |

| Common mistakes | Mixing accounts, incomplete documents, and delayed reconciliation are the most frequent and most costly errors. |

Financial records as a strategic asset, not just a compliance task

Most business owners treat recordkeeping as something they do for the tax authority. That framing is understandable, but it is also limiting. Treating documentation as business insurance transforms recordkeeping from a burden into a strategic asset. The shift in mindset is significant.

Consider what well-maintained records actually give you. They give you the evidence to win a dispute with a supplier or customer. They give you the data to identify your most profitable revenue streams. They give you the credibility to walk into a bank or investor meeting with confidence. Proper bookkeeping unlocks actionable insights, allowing founders to move beyond intuition to evidence-based growth.

The businesses that treat recordkeeping as a strategic discipline, not a compliance checkbox, are the ones that scale with clarity. They know their numbers. They can answer hard questions from investors, auditors, or partners without hesitation. That confidence is built one well-filed document at a time.

The practical recommendation is to start treating your financial records the way you treat your business contracts: as documents that protect you, inform you, and represent your business’s integrity. Build the system now, maintain it consistently, and the returns compound over years.

How Bizsquare helps Singapore businesses maintain financial records

Bizsquare provides professional accounting and bookkeeping services tailored to the compliance requirements and growth goals of Singapore businesses. From setting up your chart of accounts to managing monthly reconciliations and preparing IRAS-ready financial statements, Bizsquare’s team handles the detail so business owners can focus on operations. For startups and SMEs that need structured financial management from day one, startup bookkeeping services provide a cost-effective path to compliance and financial clarity. Contact Bizsquare today to discuss a recordkeeping solution built for your business.

FAQ

1.) Why do businesses need to maintain financial records?

Businesses need financial records to comply with IRAS and ACRA requirements, support accurate tax filing, and make informed management decisions. Poor records expose businesses to penalties, denied deductions, and failed financing applications.

2.) How long must Singapore businesses keep financial records?

IRAS requires businesses to retain records for a minimum of five years after the relevant Year of Assessment. CPA professionals recommend seven years to cover extended audit and dispute windows.

3.) What documents are considered proper financial records?

Proper financial records include sales invoices, purchase receipts, bank statements, payroll records, CPF contribution histories, contracts, GST records, and payment confirmations. Each transaction should have a complete documentary chain.

4.) What happens if a business has poor financial records?

Poor financial records can result in disallowed tax deductions, IRAS penalties, failed loan applications, and extended audits. Cash flow mismanagement linked to poor documentation accounts for approximately 82% of small business failures.

5.) How can a small business improve its financial recordkeeping?

A small business should use dedicated accounting software such as Xero or QuickBooks, separate business and personal accounts, reconcile bank statements weekly, and store documents in a centralized cloud system with access controls.

6.) Is it necessary to hire an accountant for financial recordkeeping?

Hiring a professional accountant or outsourced bookkeeper is not legally required, but it significantly reduces errors, improves compliance, and frees the business owner to focus on growth rather than administrative tasks.

7.) What is the difference between bookkeeping and accounting?

Bookkeeping is the systematic recording of daily financial transactions, while accounting involves interpreting, classifying, and reporting those records for decision-making and compliance. Both are necessary for a complete financial management system.

8.) Can digital records replace paper records in Singapore?

Yes, IRAS accepts digital records provided they are accurate, complete, and retrievable for audit purposes. Businesses must maintain backups and ensure digital files are not altered after creation.

9.) What are the most common financial recordkeeping mistakes?

The most common mistakes include mixing personal and business finances, keeping incomplete documents, delaying reconciliation, ignoring retention requirements, and failing to back up digital records.

10.) How do financial records help with business growth?

Clean financial records reveal profitable revenue streams, support financing applications, improve pricing decisions, and provide the data needed for evidence-based growth planning rather than guesswork.

11.) Does ACRA require businesses to maintain financial records?

Yes, ACRA requires Singapore-incorporated companies to maintain proper accounting records that sufficiently explain the company’s transactions and financial position, in line with the Companies Act.

12.) What is the best accounting software for Singapore SMEs?

Xero, QuickBooks, and MYOB are widely used by Singapore SMEs. These platforms integrate with local bank feeds, support GST reporting, and create automatic audit trails that simplify compliance.

13.) How often should a business reconcile its financial records?

Weekly reconciliation is the recommended practice to catch errors and fraud early. Monthly reconciliation is the minimum acceptable standard for most Singapore SMEs.