What Is Cash Flow Management for Singapore Businesses

Overview

Effective cash flow management involves monitoring and controlling the timing of money entering and leaving a business to maintain liquidity. It primarily relies on tracking operating, investing, and financing cash flows, with a focus on building reserves and negotiating payment terms. Regular analysis and real-time visibility help businesses prevent shortfalls and support growth decisions.

Cash flow management is defined as the ongoing process of tracking and controlling the timing of money moving into and out of a business to maintain liquidity and meet short-term obligations. Net cash flow equals total inflows minus total outflows. A positive result means more money enters the business than leaves it. For Singapore entrepreneurs and business owners, this discipline separates companies that grow steadily from those that collapse despite showing accounting profits. Bizsquare works with local businesses daily and sees this distinction play out in real financial outcomes.

What is cash flow management and why does it matter?

Cash flow management is the practice of monitoring, analyzing, and adjusting the timing of cash receipts and payments. The industry also refers to this as liquidity management, and both terms describe the same core discipline. The goal is simple: make sure enough cash is available to pay expenses, meet payroll, and fund growth, at every point in time.

Profit and cash availability are not the same thing. A business can show strong net income on its profit and loss statement while running out of cash to pay suppliers. This happens because accounting profit records revenue when it is earned, not when cash actually arrives. Cash flow management closes that gap by focusing on when money physically moves.

The importance of cash flow extends beyond daily operations. Businesses with healthy liquidity avoid expensive emergency credit lines, negotiate better payment terms with suppliers, and invest in growth at the right moment. For Singapore SMEs operating in a competitive market, this financial discipline is not optional. It is the foundation of operational stability.

What are the main components and types of cash flow?

Cash flow divides into three distinct categories, and each one tells a different story about a business’s financial health.

Operating cash flow covers the money generated by core business activities. This includes:

- Cash inflows: sales revenue, customer payments, service fees

- Cash outflows: payroll, rent, utilities, supplier payments, GST remittances to the Inland Revenue Authority of Singapore (IRAS)

Investing cash flow tracks money spent on or received from long-term assets. Examples include purchasing equipment, acquiring property, or selling a business vehicle. Negative investing cash flow is not always a warning sign. It often signals that a business is spending on assets that will generate future returns.

Financing cash flow records transactions with lenders and investors. Loan drawdowns, equity injections, and dividend payments all appear here. A Singapore business that takes an Enterprise Development Grant (EDG) loan would record that receipt under financing activities.

Understanding cash flow categories helps business owners monitor performance and forecast liquidity needs accurately. Net cash flow is the sum of all three categories. A business can have strong operating cash flow but negative net cash flow if it is repaying large loans simultaneously. Tracking each category separately reveals where the pressure actually comes from.

Pro Tip: Review all three cash flow categories monthly, not just operating cash. A sudden drop in financing cash flow often signals a loan repayment cycle that will squeeze your operating budget within 60 days.

How to effectively manage cash flow: strategies and best practices

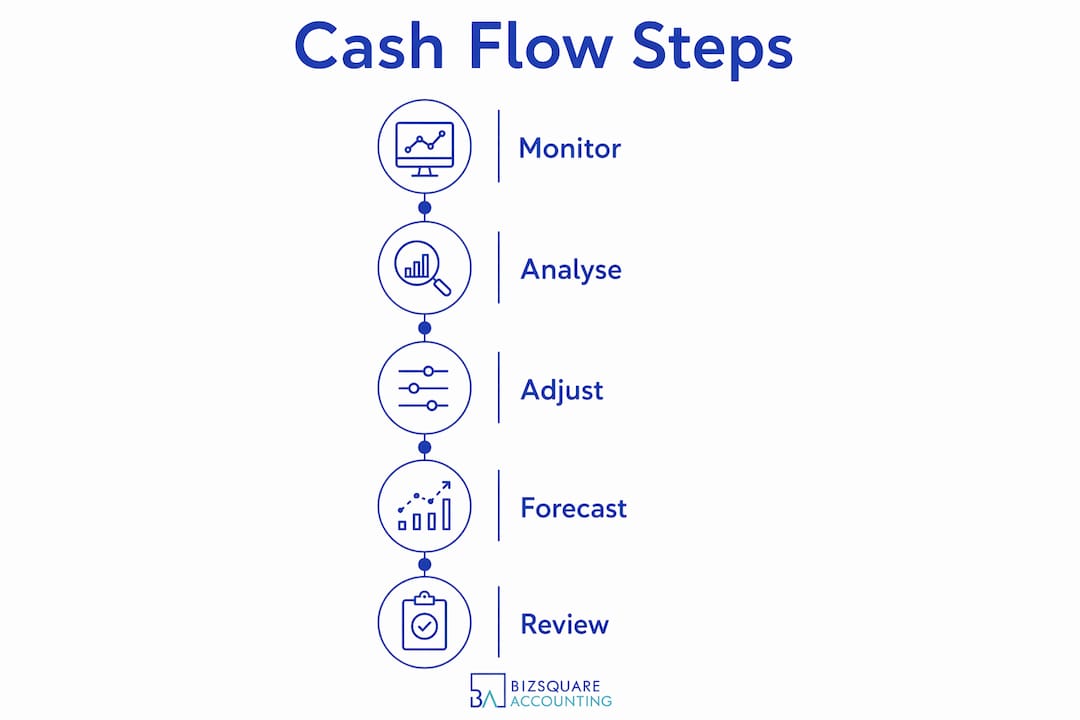

Effective cash flow management follows a structured cycle. The five steps below form the foundation of that cycle, and each one builds on the previous.

- Build a cash flow budget. Project expected inflows and outflows for the next 3–12 months. Use historical data from your accounting records as the baseline. Singapore businesses should factor in GST payment cycles, which fall quarterly for most registered companies.

- Track cash in real time. Digital accounting tools automate cash tracking, schedule payment alerts, and flag low cash positions before they become crises. Real-time visibility removes the guesswork from daily financial decisions.

- Build and maintain a cash reserve. Cash reserves equal to three months of operating expenses protect a business against unexpected revenue drops or sudden expense spikes. This reserve is the primary buffer that keeps operations running during financial stress. A Singapore retail business with $30,000 in monthly expenses should hold at least $90,000 in accessible reserves.

- Accelerate receivables and manage payables. Send invoices immediately after delivering goods or services. Offer early payment discounts using terms like “2/10 net 30,” which means the customer gets a 2% discount for paying within 10 days instead of 30. Negotiating payment terms this way compresses the cash conversion cycle and reduces working capital pressure. On the payables side, negotiate longer payment windows with suppliers without incurring penalties.

- Review and adjust periodically. Compare actual cash flow against your budget every month. Identify variances, trace their causes, and adjust the next period’s forecast. This step turns cash flow management from a reactive exercise into a proactive one.

Pro Tip: Set a fixed day each month, say the 5th, to review your cash position against your budget. Consistency matters more than the tool you use. A disciplined monthly review catches problems 30–60 days before they become emergencies.

For Singapore businesses, the local regulatory environment adds specific timing pressures. Corporate tax installments, CPF contributions due on the 14th of each month, and quarterly GST filings all create predictable cash outflows. Building these dates into your cash flow budget prevents last-minute scrambles for liquidity.

Common misconceptions and pitfalls in cash flow management

The most damaging misconception in business finance is that profit equals cash. It does not. Profitability does not guarantee that cash is available when bills come due. A Singapore consultancy that invoices $200,000 in december but collects payment in february has a profitable quarter on paper and a cash shortage in january.

Common cash flow mistakes include:

- Ignoring timing mismatches. Receivables due in 60 days cannot pay a supplier invoice due in 15 days. Many business owners see a healthy order book and assume cash will follow automatically.

- Neglecting cash reserves. Operating without a reserve means any unexpected expense, a broken server, a delayed client payment, or a regulatory fine, forces the business to seek emergency credit at high interest rates.

- Misreading accounting reports. A profit and loss statement shows revenue and expenses on an accrual basis. It does not show when cash actually arrives. Business owners who rely solely on P&L reports miss the real cash picture.

- Over-investing during strong periods. A profitable quarter tempts business owners to expand aggressively. Spending cash reserves on growth during a peak period leaves the business exposed when revenue normalizes.

- Ignoring payment term negotiations. Accepting default 30-day or 60-day payment terms from large clients without pushing back extends the cash conversion cycle unnecessarily.

“Tracking cash inflows and outflows prevents liquidity shortfalls and reduces the need for emergency credit lines. Break-even cash flow, the point where revenue covers total expenses in a period, is a more immediate measure of financial health than accounting profit.”

Real-time cash visibility using automated digital tools allows business owners to identify shortfalls early and take corrective action before the situation becomes critical. Proactive management, not reactive firefighting, is the standard that separates financially stable businesses from those that struggle.

How can cash flow analysis support business decisions?

Cash flow analysis is the process of examining historical and projected cash flow data to identify trends, detect problems, and guide decisions. Regular cash flow analysis guides smarter business decisions and better timing of growth initiatives. It turns raw financial data into a decision-making tool.

The cash flow statement is the primary document for this analysis. It shows operating, investing, and financing activities for a specific period. Reading it alongside the balance sheet and income statement gives a complete picture of financial health.

Two ratios are particularly useful for Singapore business owners:

| Ratio | Formula | What it tells you |

|---|---|---|

| Operating cash flow ratio | Operating cash flow ÷ current liabilities | Measures ability to cover short-term debts with operating cash |

| Cash flow margin | Operating cash flow ÷ net revenue | Shows how efficiently revenue converts to actual cash |

| Cash conversion cycle | Days receivable + days inventory – days payable | Measures how long cash is tied up in the business cycle |

A low operating cash flow ratio signals that the business cannot cover its short-term obligations from operations alone. That is a warning to reduce expenses, accelerate collections, or secure a credit facility before the gap widens.

Effective cash flow management also enables better timing of growth investments. When inflows are consistently strong and reserves are full, that is the right moment to hire, expand, or invest in new equipment. Waiting for that signal prevents businesses from overextending during uncertain periods.

Pro Tip: Build a 13-week rolling cash flow forecast. Update it every week with actual figures. This short-term view catches problems that a monthly or quarterly budget misses entirely, especially for businesses with irregular revenue cycles.

For Singapore businesses with seasonal revenue patterns, such as retail businesses peaking during the year-end holiday season or F&B operators seeing slower months in the first quarter, cash flow forecasting is especially critical. It allows owners to plan staffing, inventory purchases, and marketing spend around actual cash availability rather than projected profit.

Key Takeaways

Effective cash flow management requires tracking all three cash flow categories, maintaining a three-month cash reserve, and reviewing actual versus budgeted cash positions every month without exception.

| Point | Details |

|---|---|

| Cash flow is not profit | A business can be profitable on paper and still run out of cash due to timing mismatches. |

| Three cash flow categories | Operating, investing, and financing activities each reveal a different dimension of financial health. |

| Three-month cash reserve | Holding reserves equal to three months of expenses protects operations during revenue shortfalls. |

| Payment term negotiation | Terms like “2/10 net 30” accelerate inflows and reduce working capital pressure. |

| Monthly review discipline | Comparing actual cash against budget monthly turns reactive management into proactive control. |

Why cash flow is the metric I watch above all others

Most business owners I speak with track revenue and profit closely. Very few track cash with the same discipline. That gap is where financial trouble starts.

The businesses that survive difficult periods, whether a slow quarter, a client default, or an unexpected regulatory cost, are almost always the ones with cash reserves and a clear view of their cash position at any given moment. Profit is a lagging indicator. Cash is real time.

Singapore’s business environment adds specific pressures that make this even more critical. CPF contribution deadlines, quarterly GST filings, and annual corporate tax installments create predictable cash outflows that must be planned for. Businesses that treat these as surprises end up paying late penalties or drawing on expensive credit.

The most overlooked area I see consistently is payment term negotiation. Business owners accept whatever terms a large client proposes because they fear losing the contract. In practice, a politely negotiated 14-day payment term instead of 60 days can transform a business’s cash position without affecting the client relationship at all.

Technology has made cash flow tracking far more accessible than it was a decade ago. Digital bookkeeping services give Singapore SMEs real-time visibility into their cash position without requiring a full-time finance team. The barrier to good cash management is no longer cost or complexity. It is simply the decision to prioritize it.

For business owners who are not confident reading a cash flow statement, the right move is to get professional help rather than ignore the data. A qualified advisor can interpret the numbers, identify the risks, and recommend specific actions. That investment pays for itself quickly.

How Bizsquare helps Singapore businesses manage cash flow

Bizsquare provides accounting and bookkeeping services designed specifically for Singapore SMEs and entrepreneurs who need accurate, real-time financial data to make sound business decisions.

Bizsquare’s team tracks cash inflows and outflows, prepares monthly cash flow reports, and advises on reserve levels, invoicing practices, and payment timing. For businesses that need higher-level financial guidance, Bizsquare’s Outsourced CFO service provides strategic cash flow planning without the cost of a full-time finance director. Singapore business owners can also explore bookkeeping accuracy tips to strengthen their financial foundation from day one. Contact Bizsquare to find out how professional financial management translates directly into business stability and growth.

FAQ

1.) What is cash flow management in simple terms?

Cash flow management is the process of tracking money coming into and going out of a business to make sure enough cash is always available to cover expenses. It focuses on timing, not just total amounts.

2.) What is the difference between cash flow and profit?

Profit is revenue minus expenses on an accrual basis, recorded when transactions occur. Cash flow reflects actual money received and paid, which often happens at different times than the accounting entries.

3.) How much cash reserve should a Singapore business keep?

Financial experts advise maintaining a cash reserve equal to at least three months of operating expenses. This buffer covers unexpected costs or revenue shortfalls without requiring emergency borrowing.

4.) What are the three types of cash flow?

The three types are operating cash flow (from core business activities), investing cash flow (from asset purchases or sales), and financing cash flow (from loans and equity transactions).

5.) How often should a business review its cash flow?

A business should review its cash position monthly at minimum, comparing actual figures against the budget. High-growth or seasonal businesses benefit from a weekly 13-week rolling forecast.

6.) What is a cash flow forecast?

A cash flow forecast is a projection of expected cash inflows and outflows over a future period, typically 3–12 months. It helps business owners anticipate shortfalls and plan spending accordingly.

7.) What causes poor cash flow in a business?

Poor cash flow typically results from slow-paying customers, mismatched payment terms, insufficient cash reserves, or over-investment during strong revenue periods.

8.) How does cash flow analysis help business decisions?

Cash flow analysis identifies trends in inflows and outflows, highlights liquidity risks, and signals the right timing for growth investments. Ratios like the operating cash flow ratio and cash conversion cycle quantify these insights.

9.) What is the cash conversion cycle?

The cash conversion cycle measures how many days it takes for a business to convert inventory and receivables into cash. A shorter cycle means less cash is tied up in operations at any given time.

10.) Can a profitable business have negative cash flow?

Yes. A profitable business can have negative cash flow when customers pay slowly, when the business invests heavily in assets, or when loan repayments exceed operating cash generation in a given period.

11.) What is the “2/10 net 30” payment term?

“2/10 net 30” means a customer receives a 2% discount for paying within 10 days, with the full amount due within 30 days. This incentivizes early payment and improves the seller’s cash inflow timing.

12.) How do digital tools improve cash flow management?

Digital accounting tools automate transaction recording, generate real-time cash position reports, and alert business owners to low cash levels. This visibility allows faster, more accurate financial decisions.

13.) What is the role of bookkeeping in cash flow management?

Accurate bookkeeping records every transaction as it occurs, providing the data needed to build reliable cash flow reports and forecasts. Without accurate books, cash flow analysis is unreliable.

14.) How does Singapore’s GST cycle affect cash flow?

Singapore businesses registered for GST file quarterly returns and remit collected tax to IRAS. These quarterly outflows must be planned for in the cash flow budget to avoid liquidity pressure at filing time.

15.) What is the best first step to improve cash flow?

The best first step is to build a simple cash flow budget using the last three to six months of actual transaction data. That baseline reveals where timing mismatches occur and where reserves are insufficient.