Bookkeeping in Singapore: Compliance and Financial Clarity

Overview

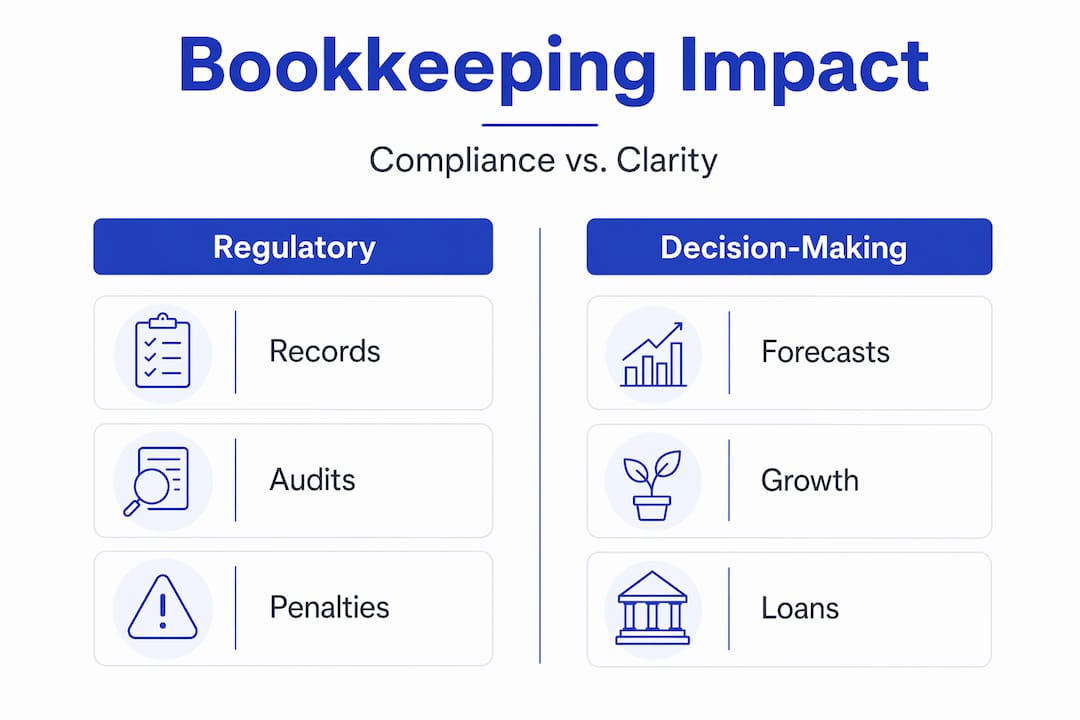

Effective bookkeeping in Singapore is vital for regulatory compliance and operational insight, supporting better decision-making and cash flow management. IRAS mandates maintaining proper records for five years, including invoices, bank statements, and payroll documents, to ensure audit readiness and avoid penalties. Building disciplined, digital recordkeeping systems early helps businesses navigate audits smoothly and leverage financial data for long-term growth.

Businesses operating in Singapore face a regulatory environment where poor financial recordkeeping carries real consequences, from tax penalties to failed audits and disrupted operations. Yet many business owners treat bookkeeping as little more than a year-end filing exercise rather than the operational backbone it truly is. This article breaks down exactly what bookkeeping requires in Singapore, how IRAS compliance obligations shape daily practice, and how systematic financial recordkeeping translates directly into better decisions, stronger cash flow management, and long-term business resilience. If you have ever wondered whether your records would survive an audit, this guide is for you.

Table of Contents

- What is bookkeeping and why does it matter?

- Singapore bookkeeping requirements: Compliance and business impact

- Bookkeeping as a foundation for smarter business decisions

- Getting started: Practical steps and expert tips for business owners

- The uncomfortable truth: Why compliance goes beyond basic bookkeeping

- Take the next step: Professional bookkeeping solutions for Singapore businesses

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Regulatory compliance | Singapore businesses must maintain accurate records for at least 5 years to meet IRAS requirements. |

| Audit readiness | Proper bookkeeping ensures easy retrieval of documents during IRAS audits, reducing penalty risks. |

| Informed decisions | Strong bookkeeping provides reliable data for business strategy, budgeting, and growth. |

| Avoiding costly mistakes | Neglecting bookkeeping can lead to missed expenses, overlooked income, and financial penalties. |

| Strategic advantage | Treating records as a strategic asset helps businesses stay prepared for broader compliance regimes. |

What is bookkeeping and why does it matter?

Bookkeeping is the systematic process of recording every financial transaction a business makes, covering sales, purchases, payments, receipts, payroll, and any other monetary activity. It is not simply data entry. Accurate bookkeeping produces the reliable financial statements and real-time visibility that allow business owners and managers to understand exactly where money is coming from, where it is going, and how much remains. This operational foundation underpins everything from daily expense approvals to strategic investment decisions.

The importance of bookkeeping for Singapore businesses extends well beyond producing year-end accounts. Consider a small manufacturing company that neglects to record supplier invoices consistently. Six months in, the owner cannot determine whether the business is profitable, which product lines are underperforming, or whether the company can afford a new piece of equipment. Without clean records, decisions default to guesswork. That is a costly way to run any business.

Bookkeeping also directly supports improving cash flow by identifying gaps between money owed and money received. Businesses that track accounts receivable and payable in real time can chase overdue invoices earlier and negotiate better payment terms with suppliers, preventing the cash crunches that cause otherwise viable companies to fail.

Here is what robust bookkeeping typically captures:

- Sales invoices issued to customers, including payment dates and amounts received

- Purchase invoices and receipts from vendors and suppliers

- Bank statements reconciled against internal records monthly

- Payroll records covering salaries, CPF contributions, and employee expense claims

- Petty cash transactions often overlooked but critical for complete accounts

- Asset registers tracking depreciation of equipment and property

- Loan and credit documentation supporting balance sheet accuracy

As the IRS records guidance confirms, bookkeeping is the operational “system of record” that produces financial statements and management visibility, covering profit and loss, balance sheet, and cash flow, used to make decisions and support financing. This principle applies equally in the Singapore context, where lenders, investors, and regulators all rely on well-maintained financial records before extending credit, capital, or approval.

“Good bookkeeping is not just a compliance exercise. It is the instrument through which a business owner gains a factual, real-time understanding of the company’s financial health and its capacity to grow.”

Implementing consistent bookkeeping alongside productivity tips for small business practices can reduce administrative burden and create more time for strategic management rather than reactive firefighting.

Now that you understand why attention to bookkeeping can make or break a business, let’s explore how regulatory obligations in Singapore shape these practices.

Singapore Bookkeeping Requirements: Compliance and Business Impact

Singapore’s regulatory framework for business recordkeeping is clear and enforceable. The Inland Revenue Authority of Singapore (IRAS) requires every business, whether a sole proprietor, partnership, or private limited company, to maintain proper accounting records that substantiate all income declared and expenses claimed. Understanding these obligations is not optional. It is the minimum standard for operating a legally compliant business in Singapore.

According to IRAS guidance on proper records, businesses must retain records for 5 years from the relevant year of assessment. This retention period applies to both digital and physical documents, and IRAS may request access to these records during an audit or compliance review at any time. Failure to produce adequate documentation can result in penalties, estimated assessments where IRAS substitutes its own figures for missing income or expense data, or even prosecution in serious cases of tax evasion.

The required documents span several categories:

- Invoices and receipts for every sale and purchase transaction

- Bank statements and reconciliation records

- Vouchers supporting internal expense approvals

- Contracts and agreements relating to business transactions

- Payroll records including CPF contribution schedules

- Asset purchase records and depreciation schedules

- Loan and lease agreements affecting liabilities and expenses

The following table outlines the key compliance requirements and the business risks associated with non-compliance:

| Compliance Requirement | Regulatory Standard | Risk of Non-Compliance |

|---|---|---|

| Retain records for minimum 5 years | IRAS requirement | Estimated assessments, fines |

| Substantiate income with invoices | IRAS requirement | Disallowed income claims |

| Support expense claims with receipts | IRAS requirement | Disallowed deductions, penalties |

| Maintain payroll and CPF records | CPF Board requirement | CPF arrears, employer penalties |

| Reconcile bank statements regularly | Best practice, audit standard | Unexplained discrepancies flagged |

| Keep records retrievable in audit | IRAS digital records guidance | Obstruction charges, penalties |

For businesses with more complex structures, including those with related-party transactions or cross-border arrangements, the IRAS tax compliance guide provides additional context on documentation standards that apply at the corporate level.

One area that many small business owners underestimate is audit readiness. IRAS audits are not solely reserved for large corporations. SMEs and sole proprietors are also subject to compliance reviews, particularly where declared income or expenses appear inconsistent with industry norms. Effective bookkeeping, as confirmed by IRAS records guidance, supports compliance and reduces friction during audits and reviews by ensuring that transactional accounting data and supporting documents are readily accessible.

Pro Tip: Establish a digital folder structure organized by financial year and transaction category. Label folders clearly (e.g., “FY2025 Purchase Invoices” or “FY2025 Bank Statements”) and back up copies to a cloud storage platform. This simple habit cuts audit preparation time dramatically and ensures you are never scrambling to locate three-year-old receipts.

When evaluating whether to manage this internally or externally, reviewing the in-house vs outsourced bookkeeping comparison can clarify which model fits your business scale, budget, and risk tolerance.

With compliance obligations top of mind, how can strong bookkeeping drive smarter business decisions and reduce operational friction?

Bookkeeping as a foundation for smarter business decisions

Beyond regulatory compliance, the most significant value of disciplined bookkeeping lies in its capacity to inform better business decisions. Reliable financial records transform management from reactive to proactive. When a business owner has accurate monthly profit and loss statements, a current balance sheet, and a clear cash flow forecast, they are equipped to make strategic calls with confidence rather than relying on intuition or incomplete data.

The connection between recordkeeping quality and decision quality is direct. As IRS records documentation articulates, bookkeeping produces the management visibility across profit and loss, balance sheet, and cash flow that supports financing and business decisions. This is equally applicable in Singapore, where banks and investors expect clean, auditable records before approving loans or funding rounds.

The contrast between weak and strong bookkeeping practices becomes especially visible during growth phases, credit applications, or business sales. The table below illustrates this directly:

| Business Scenario | Weak Bookkeeping | Strong Bookkeeping |

|---|---|---|

| Bank loan application | Delayed approval, higher scrutiny, potential rejection | Faster approval with clean financial history |

| Investor due diligence | Inability to substantiate revenue claims | Confident presentation of verified financials |

| Tax filing preparation | Last-minute scrambling, risk of errors | Accurate filing with full supporting documentation |

| Cash flow management | Surprise shortfalls and overdue obligations | Proactive management with reliable forecasts |

| Business sale or acquisition | Reduced valuation due to poor records | Full valuation supported by clean books |

| Identifying profitability | Unable to determine product or service margins | Clear margin analysis by revenue stream |

For bookkeeping for startups, establishing these foundations early is particularly important. Startups that build clean financial systems from incorporation are positioned to raise funding more easily, scale operations without administrative chaos, and transition to more sophisticated reporting structures as they grow.

Here are the concrete steps businesses can take to leverage bookkeeping for decision support:

- Reconcile bank accounts monthly. Unreconciled accounts accumulate discrepancies that distort profitability reporting and make it impossible to trust your balance sheet.

- Produce monthly profit and loss statements. Even a simple template reviewed monthly provides trend data that reveals underperforming areas before they become serious problems.

- Track accounts receivable aging reports. Understanding which invoices are overdue by 30, 60, or 90 days enables earlier intervention and protects cash flow.

- Review expense categorization quarterly. Miscategorized expenses inflate certain cost lines and can trigger scrutiny during tax reviews.

- Build a cash flow forecast using actual bookkeeping data. A 13-week rolling cash flow forecast built on real transaction history is one of the most powerful tools available to a business owner.

- Compare actuals to budgets monthly. Variance analysis between budgeted and actual figures highlights operational inefficiencies and informs where to reallocate resources.

Businesses that implement outsourcing bookkeeping through a professional provider often find that they gain not only compliance confidence but also access to analytical reporting that was previously unavailable with internal, time-constrained resources.

Applying small business tax tips alongside strong recordkeeping can also unlock deductions that under-documented businesses routinely miss, making systematic bookkeeping a direct contributor to tax efficiency.

To maximize the value, businesses can take actionable steps to implement or upgrade their bookkeeping system.

Getting started: Practical steps and expert tips for business owners

Implementing effective bookkeeping does not require a large team or an expensive system. What it requires is consistency, clarity about responsibilities, and the right tools for your business scale. Whether you are running a two-person startup or a 50-person SME, the following framework provides a practical starting point.

Audit-ready bookkeeping checklist:

- Record every transaction within 48 hours of occurrence to prevent backlog buildup

- Retain all source documents, including digital invoices, scanned receipts, and PDF bank statements

- Maintain a separate business bank account to avoid commingling personal and business funds

- Reconcile bank and credit card statements against your accounting records every month

- File VAT (GST) returns accurately and on time if your business is GST-registered

- Keep a log of asset purchases and disposals with dates, amounts, and depreciation rates

- Store all documents in a retrievable format for at least 5 years, whether digital or physical

- Back up digital records to a secure cloud platform with version history

Maintaining proper records ensures that you can retrieve transactional accounting data and supporting documents when IRAS requests them, which is the standard that every business in Singapore must meet.

Common pitfalls to avoid:

Several recurring mistakes prevent businesses from achieving reliable books. Mixing personal and business expenses is perhaps the most common error, creating reconciliation nightmares and raising red flags during audits. Delaying data entry until quarter-end or year-end turns manageable tasks into overwhelming catch-up projects prone to errors. Relying solely on bank transactions without matching them to invoices leaves gaps in the audit trail. Failing to categorize expenses consistently across periods makes trend analysis meaningless.

Choosing the right software:

Modern top bookkeeping software platforms offer cloud-based solutions that automate bank feeds, generate standard reports, and simplify GST return preparation. When evaluating options, prioritize software that supports multi-currency transactions if your business deals internationally, integrates with your payroll system, produces IRAS-compliant reports, and allows your accountant or external bookkeeper to access records remotely.

Deciding between DIY and professional bookkeeping:

The DIY vs professional bookkeeping decision depends on several factors, including transaction volume, internal financial expertise, available time, and regulatory complexity. For businesses processing fewer than 50 transactions per month with straightforward income streams, DIY bookkeeping with good software may be sufficient. For businesses with multiple revenue streams, payroll complexity, GST obligations, or cross-border transactions, professional support typically delivers better compliance outcomes and more actionable reporting.

Pro Tip: Even if you manage bookkeeping internally, schedule a quarterly review with a professional accountant. This review catches categorization errors, identifies missed deductions, and ensures your records are audit-ready well before the filing deadline.

Even with technical know-how, there’s a broader compliance trend that affects Singapore businesses. Let’s dig deeper in our editorial perspective.

Take the next step: Professional bookkeeping solutions for Singapore businesses

Navigating Singapore’s bookkeeping requirements and translating reliable financial data into actionable business decisions requires more than software alone. It demands consistent professional oversight, clear process design, and the kind of structured reporting that turns raw transactions into management intelligence.

Bizsquare provides outsourced bookkeeping services tailored to the compliance requirements and operational realities of Singapore businesses, from startups to established SMEs. Our team ensures your records are accurate, audit-ready, and structured to support both IRAS compliance and informed strategic planning. If you are evaluating your options, you can compare bookkeeping options to find the approach that aligns with your business scale, budget, and growth ambitions. Reach out to our consultants to discuss how professional bookkeeping support can reduce your compliance burden and sharpen your financial visibility.

Frequently asked questions

What documents are required for bookkeeping in Singapore?

Businesses in Singapore must maintain invoices, receipts, and vouchers along with supporting documents for all income and expense transactions, retained for a minimum of five years as required by IRAS.

What happens if my business is audited and my records are incomplete?

Incomplete or missing records expose businesses to estimated tax assessments, disallowed deductions, and penalties, because IRAS requires substantiation of all income and expense claims through retrievable documentation retained for five years.

How does bookkeeping contribute to better business decision-making?

Disciplined bookkeeping produces financial statements and management visibility across profit and loss, balance sheet, and cash flow, providing the factual foundation that enables informed decisions on budgeting, investment, and financing.

Are digital accounting records accepted by IRAS?

Yes, IRAS accepts digital records including those maintained in accounting software, provided the records can substantiate all transactions and are retrievable in a clear, organized format during audits or compliance reviews.