Singapore Incorporation: Key Benefits and Compliance Explained

Overview

– Incorporating in Singapore provides not only fast setup and attractive tax relief schemes but also establishes a governance infrastructure that supports long-term operational success.

– Ongoing compliance requirements, such as annual filings, statutory register maintenance, and appointment of a company secretary, create a disciplined framework that enhances credibility with stakeholders globally.

Most entrepreneurs who explore Singapore incorporation focus immediately on two things: how fast they can get started and how much tax they will save. While both factors are genuinely compelling, treating them as the primary reasons to incorporate misses the deeper value that Singapore’s corporate framework delivers. The real advantage lies in what happens after the certificate of incorporation is issued, the governance structure, the compliance obligations, and the operational systems that determine whether a company performs efficiently over the long term. This article walks through the evidence-backed benefits, the ongoing requirements, and the practical scenarios every founder should understand before making this decision.

Table of Contents

- Core advantages of incorporating in Singapore

- Operational and compliance requirements: More than just registration

- Tax strategy: Singapore’s flat rate and reliefs for new companies

- Special cases: Foreign founders and position-holder requirements

- Our take: Singapore incorporation is really about creating a robust business operating system

- Ready to incorporate or need help? Explore expert guidance and solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Fast digital registration | Singapore offers a streamlined online process with quick issuance of business credentials. |

| Flat tax and reliefs | The corporate income tax rate is 17% with exemptions available for new companies, boosting early-years cash flow. |

| Compliance drives efficiency | Ongoing compliance requirements like filings and AGMs are core to operational success, not just bureaucracy. |

| Foreign founder provisions | Non-residents must appoint a local director and may require nominee director services and more governance steps. |

| More than just incorporation | Successful incorporation in Singapore is about setting up a lasting governance system, not just registering for tax reasons. |

Core advantages of incorporating in Singapore

Singapore’s incorporation process is deliberately designed to reduce friction for founders. The entire registration workflow runs digitally through ACRA’s BizFile+ platform, which handles both name reservation and the formal incorporation registration, and results in the issuance of a Unique Entity Number (UEN) and a Business Profile. The UEN functions as the company’s official identifier for all government transactions, from tax filings to grant applications, making it a foundational operational asset from day one.

Speed is a genuine feature of this system. Most straightforward applications are processed within one to three business days. However, speed alone does not explain why Singapore consistently ranks among the world’s top destinations for business formation. The more substantive draw is the combination of a flat corporate income tax rate of 17% and a suite of tax relief schemes specifically designed for newly incorporated companies. For early-stage businesses, this combination can materially reduce the tax burden during the most capital-intensive years of operation.

Beyond tax, the credibility factor deserves attention. A Singapore-incorporated company carries a recognized governance standard that resonates with investors, banks, and enterprise clients both locally and internationally. Counterparties in markets across Asia, Europe, and North America are familiar with Singapore’s regulatory environment and tend to assign a higher trust premium to entities incorporated here. This is not merely a soft benefit. It translates into faster contract approvals, easier access to banking facilities, and stronger positioning in competitive procurement processes.

The following table summarizes the core advantages at a glance:

| Advantage | Practical impact |

|---|---|

| Digital incorporation via BizFile+ | Fast setup, minimal paperwork |

| Issuance of UEN and Business Profile | Enables all government and regulatory transactions |

| Flat 17% corporate income tax rate | Predictable tax planning |

| Startup tax exemption schemes | Reduced early-year tax burden |

| International credibility | Easier access to banking, investors, contracts |

For founders who want a detailed walkthrough of the process, the Singapore incorporation steps guide covers each stage systematically. Foreign entrepreneurs specifically will find the analysis of Singapore’s appeal for businesses relevant to their expansion planning.

Key benefits that experienced founders consistently highlight include:

- Regulatory clarity: Singapore’s Companies Act provides a well-defined legal framework with minimal ambiguity.

- Banking access: Incorporated companies gain access to corporate banking products and multi-currency accounts that sole proprietorships typically cannot obtain.

- Limited liability protection: Shareholders’ personal assets are legally separated from company liabilities, which is a fundamental risk management tool.

- Scalability: The corporate structure accommodates equity issuance, employee stock option plans, and institutional investment in ways that simpler business structures do not.

Operational and compliance requirements: More than just registration

Incorporation is the starting point, not the finish line. Once a company is registered, it enters an ongoing compliance cycle that directly affects its operational standing and legal good standing with ACRA. Key compliance considerations after incorporation include statutory filings and governance items such as Annual General Meetings (AGMs), annual returns, financial statement filings, and the maintenance of statutory registers. Failing to meet these obligations can result in penalties, director disqualification, or even company striking-off.

Understanding these requirements upfront allows founders to build compliance into their operational workflow rather than treating it as an afterthought. The following numbered list outlines the core ongoing obligations:

- Annual General Meeting (AGM): Private companies that qualify as small companies may be exempt from holding an AGM, but they must still circulate financial statements to shareholders within the prescribed period. Companies that do not qualify for the exemption must hold an AGM within six months of their financial year end.

- Annual return filing: Every company must file an annual return with ACRA within the prescribed timeline after the financial year end. The annual return confirms the company’s registered details, director and shareholder information, and financial position.

- Financial statement preparation: Companies are required to prepare financial statements that comply with the Singapore Financial Reporting Standards (SFRS). Smaller companies may qualify for audit exemption, but the preparation obligation remains.

- Statutory registers: Every company must maintain registers of directors, shareholders, charges, and other prescribed records. These must be kept at the registered office and made available for inspection when required.

- Company secretary appointment: A qualified company secretary must be appointed within six months of incorporation. This role carries legal responsibility for ensuring the company meets its statutory filing deadlines and governance obligations. Detailed company secretary requirements are worth reviewing before incorporation to plan for this cost.

The comparison below illustrates the difference in compliance burden between a small exempt company and a larger non-exempt company:

| Compliance item | Small exempt company | Non-exempt company |

|---|---|---|

| AGM requirement | Exempt (if qualifying) | Mandatory within 6 months of FYE |

| Audit requirement | Exempt (if qualifying) | Mandatory |

| Annual return filing | Required | Required |

| Financial statements | Required (circulated to shareholders) | Required (audited) |

| Company secretary | Mandatory | Mandatory |

“Compliance is not a bureaucratic burden, it is the governance infrastructure that protects directors, shareholders, and the company’s ability to operate without interruption.”

Pro Tip: Build a compliance calendar at the point of incorporation. Map out AGM deadlines, annual return due dates, and tax filing timelines for the first three years. This single action prevents the most common and costly compliance failures that new companies experience. Engaging corporate secretary support early ensures these deadlines are tracked and met systematically.

Staying on top of IRAS tax compliance is equally important, as tax filing obligations run in parallel with ACRA compliance and carry their own set of deadlines and penalties.

Tax strategy: Singapore’s flat rate and reliefs for new companies

Singapore’s corporate tax environment is one of the most straightforward and business-friendly in the Asia-Pacific region. The corporate income tax rate is a flat 17%, applied to chargeable income. This flat structure simplifies tax planning considerably, since companies can forecast their tax liability without navigating complex progressive rate brackets.

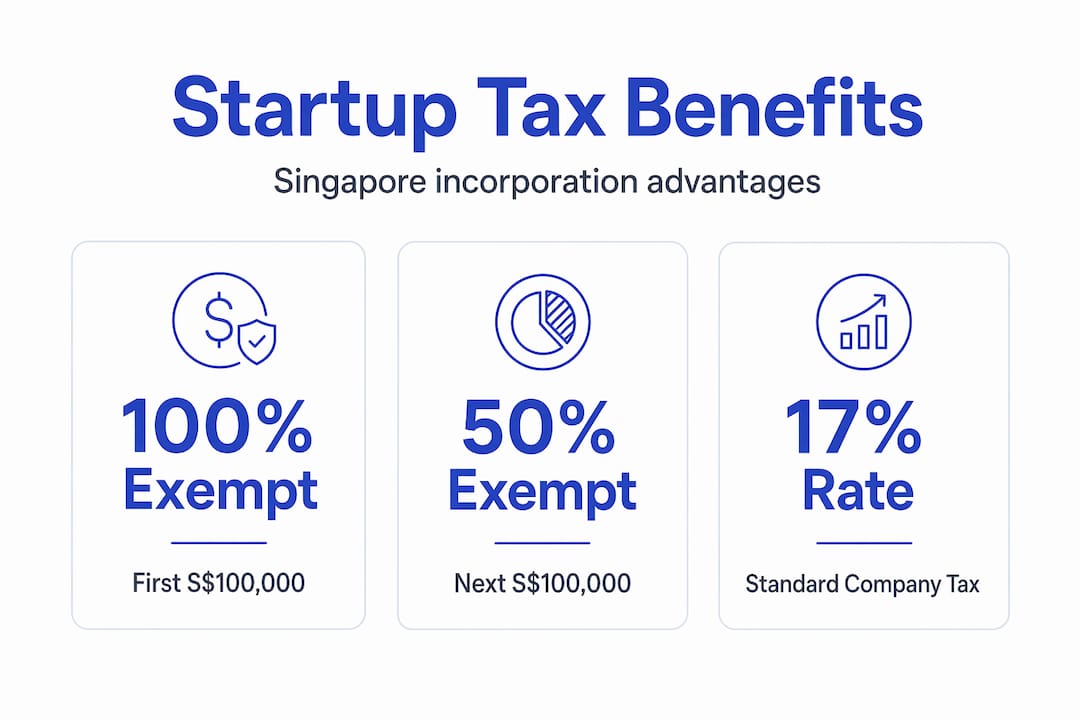

For newly incorporated companies, the Startup Tax Exemption (SUTE) scheme provides a significant reduction in the effective tax rate during the first three years of assessment. Under this scheme, qualifying companies enjoy full tax exemption on the first S$100,000 of chargeable income and a 50% exemption on the next S$100,000. This means a company generating S$200,000 in chargeable income in its first year of assessment could reduce its tax liability substantially compared to what the flat 17% rate would otherwise produce.

The following table illustrates the impact of the SUTE scheme on a company with S$200,000 in chargeable income:

| Chargeable income | Exemption | Taxable amount |

|---|---|---|

| First S$100,000 | 100% exempt | S$0 |

| Next S$100,000 | 50% exempt | S$50,000 |

| Tax at 17% on S$50,000 | S$8,500 | |

| Effective tax rate | 4.25% |

This is a material difference from the headline 17% rate and illustrates why early-stage tax planning is not optional. Companies that fail to structure their financials correctly from the start may inadvertently forfeit exemption eligibility or mistime their year-end assessments.

Beyond the SUTE scheme, Singapore also offers the Partial Tax Exemption (PTE) for companies that do not qualify for the startup exemption. Under PTE, 75% of the first S$10,000 and 50% of the next S$190,000 of chargeable income are exempt from tax. This provides a permanent baseline relief for established companies.

Key tax planning considerations for new companies include:

- Financial year end selection: Choosing the right financial year end affects when the first tax assessment falls and how much of the SUTE benefit is captured.

- Deductible expenses: Understanding which pre-incorporation and startup expenses are deductible under IRAS rules can meaningfully reduce chargeable income.

- Capital allowances: Companies investing in qualifying plant and machinery can claim capital allowances, which reduce taxable income in the years of investment.

- GST registration: Companies with taxable turnover exceeding S$1 million must register for Goods and Services Tax (GST). Voluntary registration may also be advantageous for companies with significant input tax claims.

Pro Tip: Review eligibility for the SUTE scheme before completing the incorporation registration. Certain conditions, including the requirement that the company must not be a property developer or investment holding company, affect eligibility. A corporate tax filing advisor can confirm eligibility and structure the first financial year to maximize the benefit. Foreign founders should also review the foreign company benefits analysis to understand how these reliefs interact with cross-border tax arrangements. For ongoing support, IRAS tax support resources provide practical guidance on meeting annual obligations.

Special cases: Foreign founders and position-holder requirements

Foreign entrepreneurs face an additional layer of requirements when incorporating in Singapore. The most significant is the resident director requirement. Founders who are not Singapore citizens or permanent residents must meet position-holder requirements, including the appointment of a Singapore resident director or equivalent arrangements, and may rely on licensed mechanisms such as a registered filing agent or a nominee director, which introduces additional process and governance considerations to manage.

At least one director of a Singapore company must be ordinarily resident in Singapore. This means the individual must be either a Singapore citizen, a permanent resident, or the holder of an approved work pass such as an Employment Pass or EntrePass. Foreign founders who do not meet this criterion personally must appoint a nominee director to satisfy the requirement.

The comparison below outlines the key differences between a locally resident founder and a foreign founder in terms of incorporation requirements:

| Requirement | Local founder | Foreign founder |

|---|---|---|

| Resident director | Self-qualifying | Must appoint nominee or obtain work pass |

| Registered filing agent | Optional | Often required for ACRA transactions |

| Company secretary | Mandatory | Mandatory |

| Registered Singapore address | Mandatory | Mandatory |

| Additional governance cost | Lower | Higher (nominee fees, agent fees) |

A nominee director is a licensed individual or entity that fulfills the statutory residency requirement on behalf of the foreign founder. While this arrangement is entirely legal and widely used, it carries governance risks that must be managed carefully. The nominee director has legal responsibilities as a director of the company, and any ambiguity in the nominee agreement regarding authority, liability, and indemnification can create complications during audits, banking applications, or shareholder disputes.

Key considerations for foreign founders include:

- Nominee director agreements: These should clearly define the scope of the nominee’s authority, the indemnification obligations of the foreign founder, and the conditions under which the arrangement can be terminated.

- Registered filing agent: Foreign founders who are not physically present in Singapore will typically need a registered filing agent to submit documents to ACRA on their behalf.

- Company secretary: The mandatory company secretary role is distinct from the nominee director role and must be filled by a qualified individual or corporate entity.

- Registered office address: Every Singapore company must maintain a local registered address. Virtual office services are commonly used by foreign-owned companies for this purpose.

Pro Tip: Vet nominee director agreements with the same rigor applied to any significant commercial contract. Poorly drafted agreements are among the most common sources of operational disruption for foreign-owned Singapore companies. Engaging foreign-owned compliance support from the outset reduces this risk considerably. Understanding the full scope of company secretary for foreigners obligations also helps foreign founders plan their governance structure before the first filing deadline arrives.

Our take: Singapore incorporation is really about creating a robust business operating system

The conventional narrative around Singapore incorporation focuses almost entirely on the front-end benefits: fast setup, low taxes, and a prestigious business address. These are real and meaningful. But they represent only a fraction of the value that a well-structured Singapore company delivers over its operating life.

The more accurate framing is this: incorporation in Singapore is the act of creating a governance and compliance operating system for your business. Every obligation that follows — the AGMs, the annual returns, the statutory registers, the company secretary, the tax filings — is not bureaucratic overhead. It is the infrastructure that keeps the company legally sound, financially transparent, and operationally credible to every stakeholder it will ever engage.

Experienced operators who have incorporated companies in multiple jurisdictions consistently observe that Singapore’s compliance framework, while demanding, produces companies that are better prepared for institutional investment, cross-border contracts, and eventual exit transactions. The discipline imposed by ACRA’s requirements forces a level of financial and governance hygiene that many companies in less regulated environments simply never develop.

The practical implication is that founders should treat incorporation less as a one-time tax decision and more as setting up an ongoing governance and compliance operating system. This means aligning the incorporation decision with downstream operational needs: the hiring structure, the contract framework, the audit profile, and the investor relations strategy. A company that incorporates with these downstream needs in mind will spend far less time and money correcting structural problems later.

Pro Tip: Build your compliance structure during the incorporation phase, not after. Decisions made at incorporation — financial year end, share structure, director appointments, and secretary engagement, are significantly easier and cheaper to get right the first time than to correct after the company is operational. The incorporation steps guide provides a structured framework for making these decisions in the right sequence.

Ready to incorporate or need help? Explore expert guidance and solutions

Bizsquare works with entrepreneurs and SMEs across Singapore to structure their companies for long-term operational success, not just fast registration.

Whether you are ready to start with a complete incorporation guide, need to understand your obligations around corporate secretary services, or want to get ahead of your annual obligations with a clear plan for filing corporate tax, our consultants provide the structured guidance that turns a registration into a functioning, compliant business. Contact us today to discuss your specific situation and build a governance framework that supports your growth objectives from day one.

Frequently asked questions

How long does it take to incorporate a company in Singapore?

Most standard applications are completed digitally within one to three business days through ACRA’s BizFile+, though complex cases involving referrals or additional approvals may take longer.

Do I need a company secretary after incorporation?

Yes, every Singapore company must appoint a qualified company secretary within six months of incorporation, as required under Singapore law, and this role must be maintained continuously to fulfill statutory compliance obligations.

What are the annual compliance requirements for Singapore companies?

Companies must hold AGMs (unless exempt), file annual returns, submit financial statements, and maintain statutory registers as mandated by ACRA’s compliance framework.

Can a foreign founder incorporate a Singapore company without living in Singapore?

Yes, but at least one Singapore resident director must be appointed, and foreign founders who do not qualify personally must use nominee director arrangements or obtain an approved work pass.

What is the Unique Entity Number (UEN), and why does it matter?

The UEN is the official identifier issued to every Singapore business upon registration and is used for all government and regulatory transactions, from tax filings to grant applications.