TL;DR:

- A corporate tax planning workflow is a year-round, structured process that helps businesses legally minimize tax liabilities in Singapore.

- Implementing continuous reviews, forecasts, and timely strategies ensures compliance and reduces errors, unlike reactive year-end filing.

A corporate tax planning workflow is a structured, year-round process that enables businesses to legally reduce tax liabilities while maintaining full compliance with Singapore’s Inland Revenue Authority of Singapore (IRAS) regulations. Most business owners treat tax as a once-a-year filing task, but that reactive approach costs real money. Tax planning is proactive and strategic, while year-end preparation is reactive and limited in impact. The difference between the two is the difference between controlling your tax position and simply reporting it. This guide walks business owners and financial managers through every stage of an effective corporate tax planning workflow, from foundational setup to technology integration, with practical steps built for Singapore’s regulatory environment in 2026.

What are the key components of a corporate tax planning workflow?

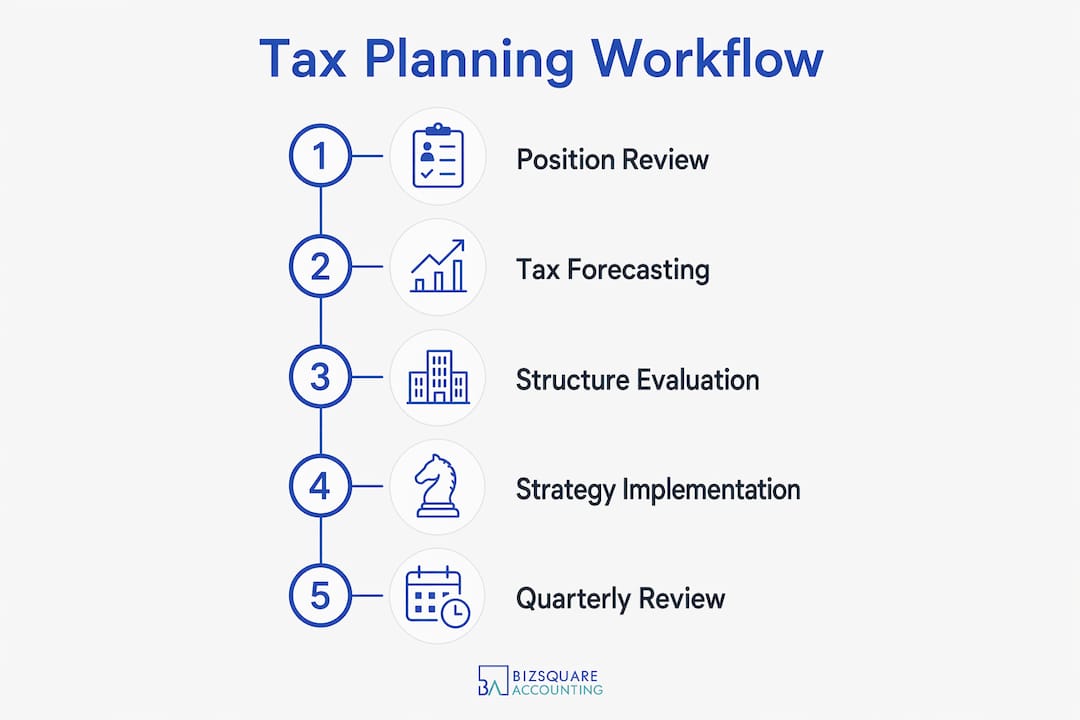

A corporate tax planning workflow is built on four core components: a current position review, multi-year forecasting, entity structure evaluation, and timely strategy implementation. This four-step process is the industry standard for proactive planning, especially for businesses with revenue exceeding $500,000. Each component feeds the next, so skipping one creates gaps that surface during audits or filing season.

The current position review covers your entity structure, compensation arrangements, projected income, and existing deductions. Multi-year forecasting models how today’s decisions affect tax liabilities two to three years forward. Entity structure evaluation asks whether your current corporate form, such as a private limited company or holding structure, still serves your tax position. Strategy implementation puts the decisions into action before deadlines expire.

Before building the workflow, business owners need three things in place: accurate financial records, access to tax advisory expertise, and a clear understanding of IRAS filing deadlines. Singapore companies must file their Estimated Chargeable Income (ECI) within three months of their financial year-end. The annual corporate tax return, Form C or Form C-S, is due by November 30 each year. Missing these dates triggers penalties that no amount of planning can recover.

The table below outlines the core tools and requirements for a functioning business tax workflow.

| Component | Tool or Resource Required | Purpose |

|---|---|---|

| Financial record-keeping | Accounting software or bookkeeper | Accurate income and expense data |

| Tax computation | Tax advisory firm or in-house tax team | Correct chargeable income calculation |

| Compliance tracking | IRAS portal, tax calendar | Meeting ECI and Form C deadlines |

| Forecasting | Spreadsheet models or ERP system | Multi-year tax liability projection |

| Documentation | Cloud storage, audit-ready filing system | Supporting claims and deductions |

Pro Tip: Set up a shared tax calendar at the start of each financial year. Mark every IRAS deadline, quarterly review date, and capital expenditure decision point. This single habit prevents most deadline-related penalties.

How to execute the core steps of the corporate tax planning workflow

Executing a corporate tax planning workflow requires discipline across the full financial year, not just the weeks before filing. Quarterly reviews help catch expiring opportunities and adjust strategies dynamically throughout the year. The following steps provide a clear sequence for business owners and financial managers to follow.

Step 1: Conduct a current position review

Start by mapping your company’s current financial position. Review your entity structure, director compensation, shareholder arrangements, and projected revenue for the year. Identify any major capital expenditures planned, as these affect depreciation claims and cash flow. This review sets the baseline for every decision that follows.

Step 2: Perform multi-year tax forecasting

Build a tax forecast that covers at least two to three years. Model different revenue scenarios, including conservative, base, and high-growth projections. Tax planning requires modeling tax impacts of key business decisions before they are finalized, especially around capital expenditures and entity restructuring. A forecast without scenario analysis is just a single guess, and a single guess is not a plan.

Step 3: Evaluate entity structure and compensation frameworks

Your entity structure directly affects your tax rate, exemptions, and filing obligations. Singapore’s corporate tax rates are capped at 17%, but newly incorporated companies qualify for partial tax exemptions under the Start-Up Tax Exemption scheme for the first three years. Review whether your current structure captures available exemptions. Evaluate director salaries and dividends to find the most tax-efficient compensation mix.

Step 4: Implement tax strategies before deadlines

Most legitimate tax reduction opportunities expire before filing season. Claim capital allowances on qualifying assets before the financial year closes. Review Section 14 deductions under the Income Tax Act for allowable business expenses. Consider accelerated depreciation for eligible assets, as front-loading deductions affects immediate cash flow but also influences future tax positions. Act on each strategy within the financial year it applies to, not after.

Step 5: Integrate quarterly and annual reviews

A quarterly review cycle is the operational backbone of effective tax planning. Each quarter, reconcile actual financials against your forecast, identify new deductions or credits, and adjust your strategy accordingly. The annual review at year-end consolidates findings, prepares documentation for IRAS submission, and resets the cycle for the next financial year.

Pro Tip: Assign a named owner for each workflow step, whether that is an internal finance manager or an external tax advisor. Workflows without clear ownership stall at the most critical moments.

What are the common challenges in a corporate tax planning workflow?

Every corporate tax planning workflow faces predictable obstacles. Identifying them early prevents costly errors and compliance failures.

The most common challenges include:

Data accuracy gaps. Incomplete or inconsistent financial records produce incorrect tax computations. Structured intake processes flag high-risk areas before running tax computations to avoid errors. Cross-border transactions, intercompany loans, and related-party arrangements need to be identified and documented before any computation begins.

Multi-jurisdictional complexity. Singapore businesses with overseas subsidiaries or regional operations face transfer pricing rules and economic substance requirements. OECD standards require demonstrating economic substance beyond paper compliance in tax jurisdictions. Profits must be taxed where actual value generation occurs, not simply where a holding entity is registered.

Regulatory changes. Singapore’s tax framework evolves annually. The 2024 introduction of the Minimum Effective Tax Rate (METR) for large multinational enterprises under the Global Anti-Base Erosion (GloBE) rules is one example. Financial managers must track IRAS updates and Budget announcements each year to adjust their workflow accordingly.

Manual errors in computation. Manual tax computations are prone to transposition errors, missed deductions, and incorrect classification of income. These errors trigger IRAS queries and, in serious cases, penalties for underreporting.

Missed deadlines. A tax compliance process without a formal calendar produces missed ECI filings and late Form C submissions. Late ECI filing results in IRAS issuing an estimated assessment, which is almost always higher than the actual liability.

Pro Tip: Before running any tax computation, complete a structured intake checklist. Flag all cross-border transactions, related-party dealings, and unusual income items for expert review. This one step prevents the majority of computation errors.

How can technology improve your corporate tax planning workflow?

Technology is the most significant force reshaping how businesses manage their tax compliance process. AI-enabled tax platforms automate data intake and audit-ready documentation, shifting finance teams from manual entry to judgment-intensive analysis. The result is faster workflows, fewer errors, and documentation that holds up under scrutiny.

Automated compliance checks

Modern tax platforms run compliance checks against current tax rules in real time. They flag deductions that exceed allowable limits, identify missing documentation, and generate alerts when filing deadlines approach. For Singapore businesses, this means ECI and Form C deadlines are tracked automatically rather than managed through manual reminders.

Scenario simulation and forecasting

Tax technology enables scenario simulations and real-time monitoring to improve forecasting and reduce errors in tax planning workflows. A financial manager can model the tax impact of a new equipment purchase, a restructuring event, or a change in director compensation before committing to the decision. This capability turns tax planning from a reporting function into a genuine decision-support tool.

Workflow automation for professional services

Document management and e-signature platforms, such as those built for professional services workflow automation, reduce the time spent routing tax documents for approval and signature. Automated workflows also create a clear audit trail, which is exactly what IRAS expects when reviewing a company’s tax position.

The table below compares key workflow features enabled by technology against traditional manual approaches.

| Workflow Feature | Manual Approach | Technology-Enabled Approach |

|---|---|---|

| Data intake | Spreadsheet entry, prone to errors | Automated import from accounting systems |

| Compliance checks | Manual review against tax rules | Real-time automated flagging |

| Deadline tracking | Calendar reminders, often missed | System-generated alerts with escalation |

| Scenario forecasting | Static spreadsheet models | Dynamic multi-scenario simulation |

| Audit documentation | Manually compiled files | Auto-generated, audit-ready documentation |

Tax technology does not replace expert judgment. It removes the administrative burden so that tax advisors and financial managers can focus on decisions that actually reduce tax liability. For Singapore SMEs that cannot justify a full in-house tax team, cloud-based platforms combined with external advisory services deliver the same capability at a fraction of the cost.

Key Takeaways

A structured, year-round corporate tax planning workflow is the most reliable way for Singapore businesses to reduce effective tax rates, maintain IRAS compliance, and make tax a financial management tool rather than an annual obligation.

| Point | Details |

|---|---|

| Plan year-round, not once a year | Quarterly reviews catch expiring opportunities that annual filing misses entirely. |

| Follow the four-step workflow | Current position review, forecasting, entity evaluation, and timely implementation form the core process. |

| Fix data quality first | Structured intake that flags cross-border and complex transactions prevents computation errors. |

| Use technology to reduce manual work | Automated compliance checks and scenario tools improve accuracy and free up advisory time. |

| Know Singapore’s key deadlines | ECI is due within three months of financial year-end; Form C or Form C-S is due by November 30. |

Tax planning is a management discipline, not a filing task

Tax is less a law knowledge issue and more a workflow coordination challenge across departments. That observation cuts to the heart of what most Singapore business owners get wrong. They treat tax as something that happens to them at year-end, rather than something they actively manage throughout the year.

The businesses that consistently pay less tax are not doing anything aggressive or legally questionable. They simply have a disciplined process. They review their position every quarter. They model decisions before committing to them. They document everything contemporaneously, not retrospectively. That discipline is available to any business, regardless of size.

The practical starting point is not a sophisticated technology platform. It is a quarterly calendar with named owners for each task. Start with that. Add a structured intake checklist. Then bring in technology and advisory support as the workflow matures. Businesses that try to implement everything at once usually implement nothing well.

Strategic tax planning elevates tax from a compliance function to a financial management lever that increases after-tax profitability. That framing matters. Tax planning done well is cash flow management. Every dollar of tax legally deferred or reduced is a dollar available for reinvestment, hiring, or debt reduction. Singapore’s tax framework, with its 17% corporate rate, Start-Up Tax Exemption, and extensive capital allowance regime, gives businesses real tools to work with. The workflow is how you use those tools consistently.

— Vandro

How Bizsquare supports your corporate tax planning

Building a disciplined tax planning process takes time, expertise, and the right advisory support. Bizsquare provides corporate tax advisory and outsourced CFO services designed specifically for Singapore SMEs, growing companies, and entrepreneurs who need structured guidance without the cost of a full in-house tax team.

Bizsquare’s tax advisory team covers the full workflow: current position reviews, multi-year forecasting, IRAS compliance management, and documentation preparation. For businesses starting from scratch, Bizsquare also handles company incorporation in Singapore, ensuring the right entity structure is in place from day one. Contact Bizsquare to schedule a consultation and build a tax planning process that works throughout the year, not just at filing time.

FAQ

What is a corporate tax planning workflow?

A corporate tax planning workflow is a structured, year-round process covering current position reviews, multi-year forecasting, entity evaluation, and timely strategy implementation to reduce tax liabilities and maintain IRAS compliance.

How often should a Singapore company review its tax position?

Singapore companies should review their tax position quarterly. Quarterly reviews catch expiring deductions and allow strategy adjustments before opportunities close.

What is the difference between tax planning and tax preparation?

Tax preparation focuses on filing past returns accurately. Tax planning models future tax impacts and aligns decisions with long-term business goals before those decisions are made.

When is the ECI filing deadline in Singapore?

The ECI must be filed within three months of a company’s financial year-end. Missing this deadline causes IRAS to issue an estimated assessment, which is typically higher than the actual liability.

What are economic substance requirements for Singapore businesses?

Economic substance requirements mandate that value-creating functions must reside in the jurisdiction where profits are declared. OECD standards require businesses to demonstrate real operational substance, not just a registered address, to avoid audit risks and additional taxes.

How does technology improve a corporate tax planning workflow?

AI-enabled tax platforms automate data intake, run real-time compliance checks, generate audit-ready documentation, and simulate multiple tax scenarios, reducing manual errors and freeing advisors to focus on decisions.

What deductions are commonly available to Singapore companies?

Singapore companies can claim capital allowances on qualifying plant and machinery, Section 14 deductions for allowable business expenses, and startup tax exemptions for the first three years of incorporation.

What is the corporate tax rate in Singapore in 2026?

Singapore’s corporate tax rate is capped at 17% of chargeable income. Newly incorporated companies qualify for partial tax exemptions under the Start-Up Tax Exemption scheme for their first three years.

What is the Form C-S filing deadline?

Form C-S and Form C are due by November 30 each year. Companies that miss this deadline face penalties and potential IRAS enforcement action.

How do I start building a corporate tax planning workflow from scratch?

Start with a quarterly tax calendar, assign named owners to each task, and complete a structured intake checklist before any computation. Add technology and external advisory support as the process matures.

What is transfer pricing, and does it affect Singapore SMEs?

Transfer pricing refers to the prices set for transactions between related entities in different jurisdictions. Singapore SMEs with overseas subsidiaries or related-party transactions must document these arrangements to comply with IRAS transfer pricing guidelines.

Can a small Singapore business benefit from corporate tax planning?

Yes. Even small businesses benefit from capital allowance claims, expense deductions, and startup exemptions. A structured tax planning approach ensures these benefits are captured consistently rather than missed at filing time.

What records does IRAS require for a corporate tax audit?

IRAS requires financial statements, tax computations, supporting invoices, contracts, and documentation for all deductions claimed. Audit-ready documentation should be maintained throughout the year, not assembled after an audit notice arrives.