What Is Tax Exemption? A 2026 Guide for Singapore Businesses

Overview

Tax exemption in Singapore completely excludes certain income, transactions, or organizations from tax liability at the source. It differs from deductions and credits by removing income from taxable calculation entirely, rather than reducing tax after assessment. Proper qualification, documentation, and accurate classification are essential to benefit from exemptions and avoid compliance issues.

Tax exemption is defined as the complete exclusion of specific income, transactions, or organizations from tax liability, meaning that excluded income is never taxed at all. This is not the same as a tax deduction or credit, which only reduce the amount of tax owed after income has already been counted. For Singapore business owners and entrepreneurs, understanding the tax exemption definition is a direct path to reducing costs legally and planning finances with precision. Singapore’s Inland Revenue Authority of Singapore (IRAS) administers a framework of exemptions that applies to startups, established companies, and qualifying non-profit organizations alike.

What is tax exemption and how does it work?

A tax exemption excludes income from the tax calculation entirely, rather than reducing it after the fact. This is the most important distinction a business owner can understand. When income is exempt, it never enters the taxable income calculation at all. This differs fundamentally from a deduction, which first counts the income and then subtracts an allowable expense.

Consider a Singapore company that receives a government grant for productivity improvement. Under IRAS rules, certain grants are classified as non-taxable receipts. The company does not include that grant in its chargeable income. The tax bill is lower not because of a deduction, but because that income never qualified as taxable in the first place.

Tax exemptions can apply to three broad categories: specific types of income, specific transactions, and specific types of organizations. A company may receive exempt income from qualifying dividends. A registered charity may be exempt from corporate income tax on income tied to its charitable purpose. A business may present an exemption certificate to a supplier to avoid paying Goods and Services Tax (GST) on qualifying purchases.

- Income-based exemptions: Certain income streams, such as qualifying foreign-sourced dividends, are excluded from Singapore corporate tax under specific conditions.

- Transaction-based exemptions: Exemption certificates are presented to sellers as proof that a transaction qualifies for tax-free treatment.

- Organization-based exemptions: Charities, Institutions of a Public Character (IPCs), and other qualifying bodies may receive full or partial exemption from income tax.

To qualify for any exemption, formal recognition or registration is typically required. IRAS does not grant exemptions automatically based on intent. The organization or income stream must meet defined criteria, and documentation must support every claim.

Pro Tip: Keep a dedicated folder, physical or digital, for every exemption-related document. This includes grant letters, IRAS correspondence, exemption certificates, and registration approvals. Clean records are the single most effective defense during an IRAS audit.

What are the main types of tax exemptions for Singapore businesses?

Singapore’s tax exemption framework covers several distinct categories. Each category has its own qualifying criteria, application process, and documentation requirements. Business owners benefit most when they understand which category applies to their specific situation.

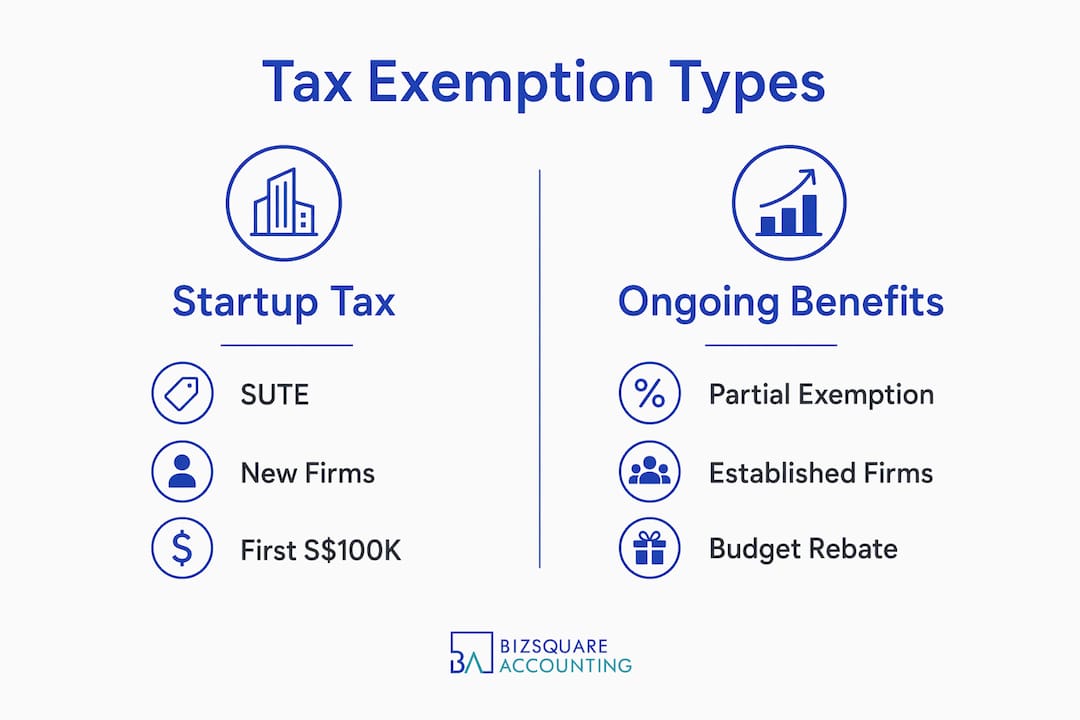

Startup tax exemption scheme

The Startup Tax Exemption (SUTE) scheme is one of the most valuable benefits for newly incorporated companies in Singapore. Under this scheme, a qualifying new company pays zero tax on the first S$100,000 of chargeable income and 50% tax on the next S$100,000, for each of its first three consecutive years of assessment. To qualify, the company must be incorporated in Singapore, tax resident in Singapore, and have no more than 20 shareholders, with at least one individual shareholder holding a minimum of 10% of shares.

Partial tax exemption for established companies

Companies that no longer qualify for SUTE move to the Partial Tax Exemption (PTE) scheme. Under PTE, 75% of the first S$10,000 of chargeable income is exempt, and 50% of the next S$190,000 is exempt. This applies to all qualifying companies regardless of age or size, making it a permanent feature of Singapore’s corporate tax structure.

Budget 2026 corporate tax rebate

Singapore’s Budget 2026 provides a 40% rebate on corporate income tax for active companies, with a minimum rebate and a capped maximum benefit. This rebate is delivered automatically starting Q2 2026, without requiring a separate application from eligible companies. This is a significant development for SMEs facing rising operational costs and intensifying competition. The rebate complements existing exemption schemes rather than replacing them.

Non-taxable income categories

Certain income types are excluded from Singapore corporate tax by statute. These include:

- Foreign-sourced dividends, branch profits, and service income remitted to Singapore, subject to conditions under Section 13(8) of the Income Tax Act.

- Capital gains, as Singapore does not impose a capital gains tax. Proceeds from the sale of investments or assets are generally not taxable.

- Specific government grants and subsidies designated as non-taxable by IRAS, such as the Productivity Solutions Grant (PSG) in certain configurations.

Exemptions for charities and non-profit organizations

Registered charities and IPCs in Singapore receive income tax exemption on income directly related to their charitable purposes. This mirrors the principle described in IRS Section 501©(3) in the United States, where organizations fulfilling religious, charitable, scientific, or educational purposes qualify for exemption. In Singapore, the Commissioner of Charities administers this recognition. Simply operating as a non-profit is not sufficient. Formal registration and ongoing compliance with the Charities Act are required.

| Exemption Type | Who Qualifies | Key Benefit |

|---|---|---|

| Startup Tax Exemption (SUTE) | New Singapore-incorporated companies, first 3 years | Zero tax on first S$100,000 of chargeable income |

| Partial Tax Exemption (PTE) | All qualifying resident companies | 75% exemption on first S$10,000; 50% on next S$190,000 |

| Budget 2026 Corporate Rebate | Active companies with local employment | 40% rebate on corporate income tax, applied automatically |

| Foreign-Sourced Income Exemption | Companies remitting qualifying foreign income | Qualifying income excluded from Singapore tax |

| Charity/IPC Exemption | Registered charities and IPCs | Full exemption on income tied to exempt purposes |

How does tax exemption differ from deductions and credits?

Tax exemption, deductions, and credits are three distinct mechanisms. Confusing them leads to filing errors and missed savings. Each operates at a different stage of the tax calculation.

Tax exemption removes income from the calculation entirely. If S$50,000 of income is exempt, it is as if that income never existed for tax purposes. The taxable base is smaller from the start.

Tax deductions reduce taxable income after it has been counted. A company earns S$500,000 in revenue. It claims S$100,000 in allowable deductions, such as staff costs, rental, and depreciation. The taxable income becomes S$400,000. The deduction did not eliminate the income. It reduced the base on which tax is calculated. For a detailed breakdown of what qualifies, the Singapore tax deductions guide from Bizsquare covers the full list of allowable expenses under IRAS rules.

Tax credits reduce the actual tax payable, not the income. After calculating tax on S$400,000, a company with a S$5,000 tax credit pays S$5,000 less in tax. Credits are applied after the tax figure is determined.

| Mechanism | What It Reduces | Stage of Calculation | Example |

|---|---|---|---|

| Tax exemption | Taxable income base | Before calculation begins | Exempt grant income never counted |

| Tax deduction | Chargeable income | During income calculation | Staff costs deducted from revenue |

| Tax credit | Tax payable | After tax is calculated | Budget 2026 rebate reduces final bill |

A common misconception among business owners is that receiving exempt income means no tax obligations exist at all. This is incorrect. Tax-exempt status covers only specific income tax obligations. A company with exempt income still pays corporate tax on non-exempt income, GST on applicable transactions, and payroll taxes on employee salaries. Exemption is targeted, not blanket.

Pro Tip: When reviewing your annual tax filing, separate income streams into three columns: fully taxable, partially exempt, and fully exempt. This simple exercise prevents the most common error, which is applying deduction logic to exempt income and vice versa.

How to qualify for and maintain tax exemptions in Singapore

Qualifying for tax exemptions in Singapore requires deliberate action, not passive eligibility. The following steps outline the process for business owners working within IRAS’s framework.

- Confirm your company’s eligibility. Review the specific criteria for each exemption scheme. For SUTE, confirm your incorporation date, shareholder structure, and tax residency status. For foreign-sourced income exemptions, verify that the income has been subject to tax in the foreign jurisdiction and that the headline tax rate there is at least 15%.

- Register with the relevant authority. Charities seeking income tax exemption must register with the Commissioner of Charities. Companies claiming foreign-sourced income exemptions must meet the conditions under Section 13(8) of the Income Tax Act. IRAS does not require a separate application for SUTE or PTE. These apply automatically when the company files its corporate tax return correctly.

- Prepare and maintain complete documentation. Tax exemptions require formal documentation, including articles of incorporation, purpose statements for non-profits, and supporting evidence for each exempt income stream. For foreign income, this means foreign tax invoices, remittance records, and confirmation of the foreign tax paid.

- File the corporate tax return accurately. The corporate tax filing process in Singapore requires companies to submit an Estimated Chargeable Income (ECI) within three months of the financial year end, followed by the full Form C or Form C-S. Exempt income must be correctly classified and excluded from the chargeable income figure.

- Avoid common compliance pitfalls. The most frequent errors include: claiming SUTE beyond the first three years of assessment, misclassifying taxable grants as non-taxable, and failing to report unrelated business income for exempt organizations. IRAS conducts regular reviews, and incorrect claims attract penalties.

- Integrate exemptions into financial planning. Tax exemptions are most valuable when factored into cash flow projections and annual budgets. A company that knows its first S$100,000 is tax-free can allocate that saving toward reinvestment, hiring, or reserves. This is not a year-end exercise. It is a planning tool used throughout the financial year.

- Engage professional accounting support. Maintaining IRAS tax compliance is significantly more reliable with professional bookkeeping and tax advisory support. Qualified accountants track changes in IRAS guidelines, identify newly qualifying income streams, and prepare documentation that withstands scrutiny. For SMEs without a full-time finance team, outsourced accounting is a practical and cost-effective solution.

Key takeaways

Tax exemption is the most powerful form of tax relief available to Singapore businesses because it removes qualifying income from the tax base entirely, unlike deductions or credits that only reduce it.

| Point | Details |

|---|---|

| Exemption removes income entirely | Exempt income is never counted in the taxable base, unlike deductions which reduce it afterward. |

| Singapore offers multiple schemes | SUTE, PTE, and the Budget 2026 rebate each serve different company stages and sizes. |

| Documentation is non-negotiable | IRAS requires formal records to support every exemption claim, especially for foreign income and charities. |

| Exemption does not eliminate all taxes | Payroll taxes, GST, and tax on non-exempt income still apply even when some income is exempt. |

| Professional support reduces risk | Qualified accountants prevent misclassification errors and keep filings aligned with current IRAS rules. |

Optimize your tax exemptions with Bizsquare

Understanding tax exemption rules is one thing. Applying them correctly within IRAS’s framework, year after year, is another challenge entirely.

Bizsquare provides expert corporate tax filing and advisory services designed specifically for Singapore SMEs, startups, and growing companies. From identifying which exemption schemes apply to your business, to preparing accurate ECI submissions and Form C filings, Bizsquare’s consultants handle the details so you can focus on running your business. Bizsquare also supports company incorporation for entrepreneurs who want to structure their business correctly from day one and maximize available tax benefits from the outset. Contact Bizsquare today to schedule a consultation.

FAQ

1.) What is the tax exemption definition in simple terms?

Tax exemption means that specific income, a transaction, or an organization is completely excluded from tax liability. The excluded income is never counted as taxable income in the first place.

2.) How does the startup tax exemption work in Singapore?

Singapore’s Startup Tax Exemption (SUTE) scheme gives newly incorporated qualifying companies zero tax on the first S$100,000 of chargeable income and 50% exemption on the next S$100,000, for the first three consecutive years of assessment.

3.) Who qualifies for tax exemption in Singapore?

Qualifying entities include newly incorporated Singapore-resident companies under SUTE, all resident companies under PTE, registered charities and IPCs for income tied to their exempt purposes, and companies receiving qualifying foreign-sourced income under Section 13(8) of the Income Tax Act.

4.) What is the difference between tax exemption and tax deduction?

Tax exemption removes income from the taxable base entirely, so it is never taxed. A tax deduction reduces chargeable income after it has been counted, lowering the amount on which tax is calculated.

5.) Does tax-exempt status mean a business pays no taxes at all?

No. Tax-exempt status covers only specific income tax obligations. A company with exempt income still pays GST on applicable transactions, payroll taxes on employee salaries, and corporate tax on any income that does not qualify for exemption.

6.) What is corporate tax exemption in Singapore?

Corporate tax exemption in Singapore refers to schemes like SUTE and PTE that exclude a portion of a company’s chargeable income from corporate income tax. The Budget 2026 rebate adds a 40% reduction on the remaining tax payable for eligible active companies.

7.) How do I apply for tax exemption with IRAS?

SUTE and PTE apply automatically when a company files its corporate tax return correctly. Foreign-sourced income exemptions require meeting conditions under Section 13(8) of the Income Tax Act. Charities must register separately with the Commissioner of Charities.

8.) What documents do I need to support a tax exemption claim?

Required documents typically include articles of incorporation, financial statements, grant letters or income source confirmation, foreign tax payment records for foreign-sourced income, and IRAS correspondence confirming any special exemption status.

9.) Can a Singapore company lose its tax exemption status?

Yes. A company loses SUTE eligibility after three years of assessment or if it no longer meets the shareholder criteria. Charities lose exemption if they fail to maintain registration or if income is generated from activities unrelated to their exempt purpose.

10.) Are government grants in Singapore tax-exempt?

Some government grants are classified as non-taxable by IRAS, such as certain productivity-related grants. Others are taxable. Business owners should verify the tax treatment of each grant with IRAS or a qualified tax advisor before excluding it from chargeable income.

11.) What is an exemption certificate and when is it used?

An exemption certificate is a document presented to a seller as proof that a transaction qualifies for tax-free treatment. It is commonly used by qualifying organizations to claim exemption from GST or other transaction-based taxes on eligible purchases.

12.) Does Singapore have capital gains tax exemption?

Singapore does not impose a capital gains tax. Gains from the sale of investments or assets are generally not taxable, making this a statutory exemption that benefits all Singapore-based businesses and investors by default.

13.) How does the Budget 2026 corporate tax rebate interact with existing exemptions?

The Budget 2026 rebate provides a 40% reduction on corporate income tax payable and is applied automatically for eligible active companies from Q2 2026. It operates on top of existing exemption schemes like SUTE and PTE, further reducing the final tax bill on chargeable income.