How to Prepare Tax Filings for Singapore Companies

Overview

– Corporate tax compliance in Singapore requires precise preparation to avoid penalties, including organized documentation and understanding IRAS expectations.

– Proper filing involves multiple steps, from document collection and validation to timely submission via designated portals, with strict adherence to deadlines.

– Maintaining good records, claiming legitimate deductions supported by documentation, and engaging professionals early help companies minimize risks and optimize tax outcomes.

Corporate tax compliance in Singapore demands precision that many business owners underestimate until a penalty notice arrives. Knowing how to prepare tax filings correctly means more than meeting deadlines. It means organizing the right documents, understanding what IRAS expects from companies of different sizes, identifying legitimate deductions, and avoiding the specific mistakes that trigger audits and surcharges. This guide provides Singapore business owners with a practical, regulation-informed walkthrough covering every stage of corporate tax preparation, from document collection to submission confirmation.

Table of Contents

- Key Takeaways

- How to prepare tax filings: documents you need first

- Steps for filing corporate tax with IRAS

- Tax deductions available to Singapore companies

- Common tax filing mistakes and how to avoid them

- My perspective on corporate tax preparation in Singapore

- How Bizsquareaccounting simplifies corporate tax filing

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Distinguish ACRA from IRAS filings | Annual returns to ACRA and corporate tax submissions to IRAS are separate obligations with different documents and deadlines. |

| Gather documents before starting | Collect financial statements, audit reports, and IRAS forms early to avoid last-minute rejections and late filing penalties. |

| Use BizFinx for XBRL filings | Companies required to submit XBRL-tagged financial statements must validate them through BizFinx before uploading to BizFile+. |

| Claim deductions with documentation | Capital allowances, R&D incentives, and business expenses are deductible only when supported by proper audit trails. |

| Disclose errors voluntarily | Self-reporting tax errors to IRAS before an investigation qualifies companies for reduced penalties under the Voluntary Disclosure Programme. |

How to prepare tax filings: documents you need first

Before a single form is completed, the quality of a company’s filing depends entirely on what has been collected and organized beforehand. Missing one document can delay the entire submission and, in some cases, result in rejection or late filing penalties. Singapore companies should treat document preparation as the foundation of the entire tax filing process.

The mandatory documents and data points typically required include the following:

- Audited or unaudited financial statements: Companies above the audit exemption threshold must submit audited accounts. Exempt private companies with revenue below S$10 million and fewer than 20 shareholders may use unaudited statements.

- Director’s report and declaration: Required as part of annual financial reporting obligations.

- IRAS Estimated Chargeable Income (ECI) form: Must be filed within three months of the financial year end unless the company qualifies for an ECI filing waiver.

- Form C-S, Form C-S (Lite), or Form C: The correct form depends on company revenue and complexity. Companies with annual revenue of S$5 million or less may use Form C-S or Form C-S (Lite).

- Supporting schedules: Depreciation schedules, capital allowance workings, and director fee schedules are commonly required to substantiate declarations.

For companies required to file financial statements in XBRL format, the XBRL tagging and validation process via BizFinx is mandatory to produce machine-readable data for ACRA. This is separate from the IRAS tax submission itself, and failing to validate correctly before upload causes rejection.

Accessing the relevant portals requires CorpPass for company-level authentication and Singpass for individual identity verification. Directors and authorized staff should confirm their CorpPass access is active and linked to the correct Unique Entity Number well before the filing period opens.

Pro Tip: Start collating financial records at least 60 days before your filing deadline. Waiting until the final two weeks to gather statements, reconcile accounts, and run XBRL validation creates unnecessary pressure and increases the likelihood of submission errors that trigger penalties.

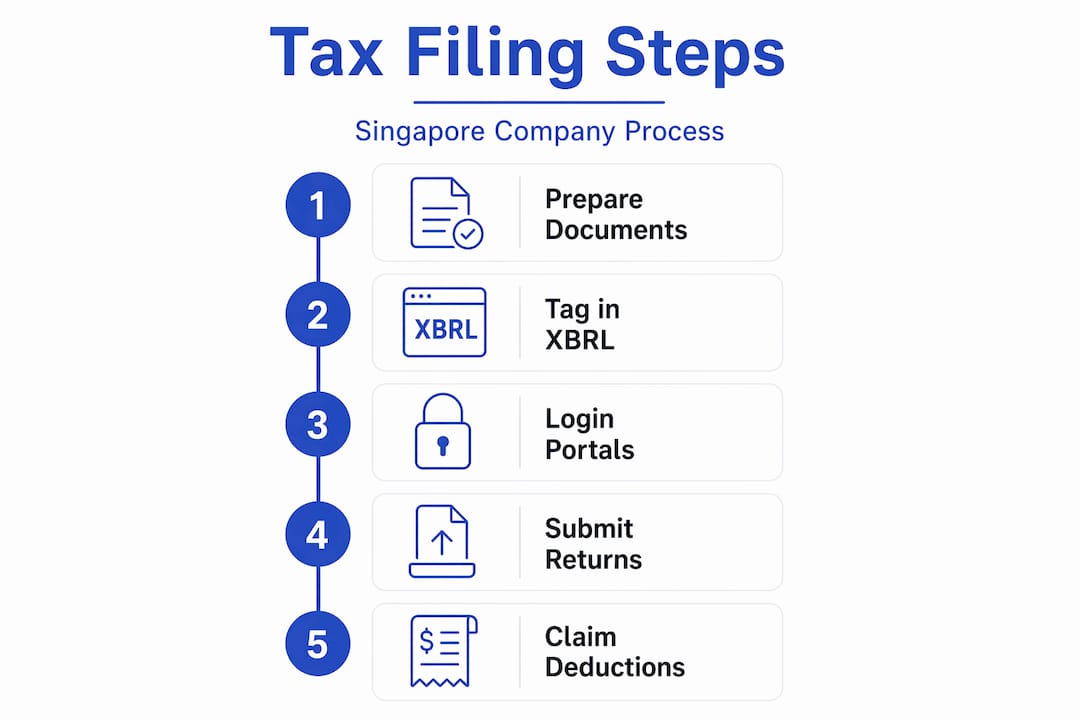

Steps for filing corporate tax with IRAS

Once all documents are in order, the actual filing process follows a defined sequence. Skipping steps or completing them out of order is one of the more common causes of rejected submissions. The following walkthrough reflects the standard process for Singapore-incorporated companies.

- Confirm your financial year end (FYE). IRAS filing deadlines are tied to the FYE. Form C, Form C-S, and Form C-S (Lite) are due by 30 November of the year of assessment for paper filings, and 15 December for e-filings. ECI must be filed within three months of the FYE.

- Determine your audit requirement. Companies that do not qualify for audit exemption must have their financial statements audited by a registered public accountant before filing. Submitting unaudited statements when audited ones are required is a compliance violation.

- Prepare financial statements and tag them in BizFinx if required. Companies required to submit XBRL-tagged statements must use the BizFinx preparation tool to tag and validate before uploading. Familiarity with XBRL tagging conventions matters here. A misapplied tag causes validation failure and requires resubmission.

- Log in to BizFile+ and complete the annual return. The annual return to ACRA is filed through BizFile+. This is a statutory obligation under the Companies Act and is distinct from the IRAS corporate tax submission. Annual returns and tax filings are separate processes with different documents and timelines. Non-listed companies have seven months from their FYE to file the annual return.

- File corporate income tax with IRAS via myTax Portal. Log in using CorpPass, select the correct form (C, C-S, or C-S Lite), complete all fields, and attach supporting schedules. Verify that the accounting standards declared in your financial statements match what is stated on the form. A mismatch between statements and declared standards is a documented cause of resubmission requests from IRAS.

- Confirm submission and retain acknowledgment. After submitting, download and store the IRAS submission acknowledgment. This is your legal record of compliance for that year of assessment.

The table below summarizes the key filing deadlines and form types for reference.

| Filing Obligation | Due Date | Platform |

|---|---|---|

| Estimated Chargeable Income (ECI) | Within 3 months of FYE | IRAS myTax Portal |

| Form C-S / C-S Lite / Form C (e-filing) | 15 December of year of assessment | IRAS myTax Portal |

| ACRA Annual Return (non-listed companies) | Within 7 months of FYE | BizFile+ |

| XBRL Financial Statements | Same as annual return | BizFile+ via BizFinx |

Late submission of tax filings results in penalties and interest charges that can significantly increase costs for the year. Starting preparation early and following these steps in order is the most reliable way to avoid that outcome.

Tax deductions available to Singapore companies

Singapore’s corporate tax framework is genuinely favorable compared to most jurisdictions, with a headline rate of 17% and multiple legitimate mechanisms for reducing taxable income. However, deductions are not automatic. They must be substantiated, correctly categorized, and declared in the appropriate section of the tax form.

The most commonly applicable deductions and credits for Singapore companies include:

- Revenue expenses incurred in producing income: Salaries, rent, utilities, marketing costs, and professional fees are generally deductible as long as they are incurred wholly and exclusively in the production of income. Personal expenses passed through the company are a frequent audit trigger.

- Capital allowances: Businesses can claim allowances on fixed assets such as machinery, computers, and office equipment under Section 19 or 19A of the Income Tax Act. These replace the concept of depreciation for tax purposes.

- Research and development (R&D) incentives: Qualifying R&D expenditure may be eligible for enhanced deductions under the R&D Tax Incentive scheme, which allows companies to claim more than the actual amount spent under specific conditions.

- Startup tax exemptions: Companies incorporated in Singapore and tax resident here may benefit from tax exemption on the first S$100,000 of chargeable income for the first three years of assessment, with a 50% exemption on the next S$100,000.

- Double tax deductions: Certain international business development costs and investment promotion expenses qualify for double tax deductions under specific IRAS-approved schemes.

Maintaining proper documentation and audit trails is not optional when claiming deductions. IRAS may request supporting records at any point, and an inability to produce them can result in the disallowance of the deduction along with additional assessments. Professional accounting services that maintain records aligned with IRAS requirements significantly reduce this risk.

One area that companies frequently overlook is transfer pricing. If the business engages in transactions with related parties, such as a parent company, subsidiary, or associated company, those transactions must be conducted at arm’s length and supported by contemporaneous documentation. Missing transfer pricing documentation may lead to a 5% surcharge on tax adjustments, in addition to any tax assessed by IRAS.

If errors or underreported income are discovered after filing, acting quickly matters. Companies that self-disclose tax errors before an IRAS investigation begins qualify for reduced penalties under the Voluntary Disclosure Programme. Waiting until an audit is initiated can result in the maximum applicable surcharges.

Pro Tip: For deductions involving R&D, intellectual property, or related-party transactions, engage a tax advisory professional before filing rather than after. Complex deduction categories carry a higher audit risk, and a qualified advisor can structure the claim and documentation in ways that withstand scrutiny.

Common tax filing mistakes and how to avoid them

Even financially experienced business owners make recurring errors when preparing corporate tax filings. Most of these mistakes are not the result of dishonesty. They stem from misunderstanding how the Singapore compliance framework operates, which has multiple parallel obligations that look similar on the surface but operate very differently.

The most consequential mistakes fall into several categories:

- Confusing ACRA and IRAS obligations: One of the most frequently observed compliance failures is treating the annual return to ACRA as equivalent to corporate income tax filing with IRAS. Annual returns and corporate tax filings are separate processes with different documents and timelines, and missing either one has distinct legal consequences.

- Submitting documents in incorrect formats: BizFile+ and myTax Portal have specific format requirements. For instance, XBRL submissions that fail BizFinx validation cannot be uploaded. PDF documents uploaded in the wrong file structure are rejected without warning. These format errors often surface only at the point of submission, when deadlines are already close.

- Omitting or misrepresenting related-party transactions: Companies engaged in intercompany loans, management fee arrangements, or cross-border service agreements frequently underestimate how carefully IRAS reviews these. The 5% surcharge on transfer pricing adjustments is an additional cost that applies on top of the tax owed, not in place of it.

- Claiming personal expenses as business deductions: Expenses that serve a dual purpose, or are primarily personal, are not deductible. IRAS scrutinizes entertainment, travel, and vehicle-related expenses in particular.

- Filing without verifying declarations: Submitting a form that contradicts the financial statements attached to it is a common cause of IRAS queries. Verification of financial statements matching accounting standards must happen before submission, not after.

“Tax risk management improves organizational controls around tax filings. IRAS encourages voluntary compliance through CTRM frameworks that reduce penalties and support a cooperative relationship between businesses and the authority.”

Before submitting any tax filing, companies should run through a pre-submission checklist: verify that financial statements reconcile with the income declared, confirm all deductions have supporting documentation, check that related-party transactions are disclosed and priced correctly, and confirm the correct form type has been selected based on current-year revenue. The financial year end compliance checklist maintained by Bizsquareaccounting is a useful reference for businesses working through this verification process.

How Bizsquare simplifies corporate tax filing

Preparing corporate tax filings in Singapore requires more than completing a form. It requires accurate books, correctly formatted documents, and an understanding of IRAS rules that applies to your specific company structure and financial position.

Bizsquare provides end-to-end corporate tax filing and advisory services for Singapore companies, covering ECI preparation, Form C-S and Form C submissions, XBRL financial statement tagging, transfer pricing documentation, and voluntary disclosure guidance. The firm’s accounting and bookkeeping services are structured to align monthly recordkeeping with IRAS filing requirements, so businesses arrive at filing season with organized, compliant records rather than a backlog. For business owners who want to reduce compliance risk and optimize their tax position without handling the complexity in-house, Bizsquare offers the professional depth to make that possible. Contact the team to discuss your company’s specific filing requirements.

FAQ

What documents are needed to file corporate taxes in Singapore?

Companies typically need audited or unaudited financial statements, the appropriate IRAS form (C, C-S, or C-S Lite), ECI calculations, and supporting schedules for deductions such as capital allowances. XBRL-tagged financial statements are also required for companies above certain thresholds.

What is the difference between ACRA and IRAS filings?

The ACRA annual return is a statutory filing under the Companies Act submitted through BizFile+, while the IRAS corporate tax filing is a separate income tax obligation submitted through myTax Portal. Both have different documents, deadlines, and consequences for non-compliance.

How do Singapore companies reduce their corporate tax liability?

Legitimate methods include claiming capital allowances on fixed assets, deducting qualifying business expenses, applying for startup tax exemption schemes, and utilizing R&D incentives. All deductions must be supported by proper documentation and disclosed correctly on the tax form.

What happens if a company files its tax return late?

Late tax filings result in financial penalties and interest charges imposed by IRAS. Repeated late filings can also result in IRAS issuing a Notice of Assessment based on estimated income, which the company must then dispute with documentation.

What is Singapore’s Voluntary Disclosure Programme?

The Voluntary Disclosure Programme allows companies that discover tax errors to self-report to IRAS before an audit begins. Companies that do so qualify for reduced penalties compared to errors discovered through IRAS investigation. Acting before IRAS initiates contact is a material factor in penalty calculation.