What Is Bookkeeping? Guide for Singapore Business Owners

Overview

– Many Singapore entrepreneurs overlook bookkeeping, risking compliance penalties and financial mismanagement.

– Good bookkeeping practices ensure accurate records, timely filings, and better financial decisions that support growth.

Many Singapore entrepreneurs treat bookkeeping as an afterthought, something to sort out at year end when the accountant calls. That instinct is costly. Understanding what is bookkeeping, in precise and practical terms, is the first step toward protecting your business from compliance penalties, cash flow surprises, and poor financial decisions. Bookkeeping is not accounting, and confusing the two leads to gaps that can sink an otherwise healthy company. This guide explains the bookkeeping definition clearly, covers Singapore’s legal requirements, and shows how good financial habits translate directly into better business outcomes.

Table of Contents

- Key Takeaways

- What is bookkeeping and why it matters

- Singapore’s bookkeeping compliance requirements

- Modern bookkeeping tools and software

- Common bookkeeping mistakes to avoid

- How bookkeeping data drives better decisions

- My perspective on bookkeeping as a strategic discipline

- How Bizsquareaccounting supports your bookkeeping needs

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Bookkeeping vs. accounting | Bookkeeping records daily transactions; accounting interprets that data to guide strategy. |

| Singapore’s 7-year rule | Companies Act Section 199 mandates retaining all accounting records for at least seven years. |

| Software reduces errors | Cloud platforms automate reconciliation and GST filing, cutting manual mistakes significantly. |

| Common pitfalls are avoidable | Mixing personal and business finances, and missing source documents, are the top causes of compliance issues. |

| Books drive decisions | Accurate, timely bookkeeping data supports cash flow forecasting, tax planning, and growth choices. |

What is bookkeeping and why it matters

At its core, bookkeeping is the systematic process of recording, organizing, and maintaining every financial transaction a business makes. Sales invoices, supplier payments, payroll entries, bank deposits — each of these must be captured accurately and consistently. Without that discipline, no meaningful financial picture can emerge.

The bookkeeping definition becomes clearer when you separate it from accounting. Bookkeeping handles the raw data: the daily input of figures into ledgers, journals, and reconciliation sheets. Accounting takes that data and transforms it into analysis, forecasting, and strategic guidance. Bookkeeping enables accounting through accurate data capture — without clean books, no accountant can deliver reliable advice.

For small businesses in Singapore, the daily mechanics of bookkeeping typically include:

- Sales journals: Recording every revenue transaction, including invoice date, customer name, and amount received.

- Purchase journals: Tracking supplier invoices, payment terms, and amounts owed or settled.

- Payroll records: Documenting salaries, CPF contributions, and related deductions for each pay period.

- Cash books: Capturing all cash and bank transactions as they occur.

- Accounts receivable and payable ledgers: Monitoring who owes you money and what you owe others.

The bookkeeping structure built from journals, ledgers, and cash books serves as the master financial record from which all financial statements are compiled. Think of it as the foundation that everything else stands on. A business with disorganized books cannot produce a reliable profit and loss statement, cannot file GST accurately, and cannot present clean financials to a bank or investor when it matters most.

Singapore’s bookkeeping compliance requirements

Singapore’s regulatory framework for bookkeeping is specific and non-negotiable. Business owners who treat record-keeping casually face real legal exposure, not just administrative inconvenience.

Here are the core compliance obligations every Singapore company must meet:

- Maintain sufficient accounting records. Under Companies Act Section 199, every company must keep records that adequately explain its financial transactions, enable the preparation of financial statements, and allow auditors to verify those statements.

- Retain records for a minimum of seven years. All accounting records and supporting source documents must be kept for at least seven years from the date of the transaction or the end of the financial year to which they relate. This applies to both digital and physical records.

- Maintain a traceable audit trail. Every figure in a financial statement must be traceable back to its original source document, whether that is a sales invoice, a bank statement, or a payment receipt. Missing traceability leads to disallowed transactions during audits and potential penalties from IRAS.

- Handle GST records properly. GST-registered businesses must maintain tax invoices, credit notes, and import documents. These must align exactly with the GST returns filed with IRAS each quarter. Errors here trigger audits and surcharges.

- Preserve source documents. Bank statements, invoices, receipts, contracts, and delivery orders all qualify as source documents. Losing them, even accidentally, weakens your audit trail and your legal position.

| Record type | Retention period | Format accepted |

|---|---|---|

| Accounting records (ledgers, journals) | 7 years minimum | Digital or physical |

| Source documents (invoices, receipts) | 7 years minimum | Digital or physical |

| GST tax invoices and credit notes | 5 years (IRAS requirement) | Digital or physical |

| Payroll and CPF records | 5 years minimum | Digital or physical |

Pro Tip: Scan and store all physical receipts in a cloud folder organized by month and category. Physical paper fades, gets lost, and creates bottlenecks during audits. A consistent digital filing system costs nothing but time and saves considerable stress.

The importance of bookkeeping services for regulatory compliance cannot be overstated in Singapore’s audit environment. IRAS and ACRA both conduct reviews that rely entirely on the quality of a company’s financial records.

Modern bookkeeping tools and software

Understanding what is bookkeeping software helps business owners move from manual, error-prone spreadsheets to systems designed for speed and accuracy. Cloud-based accounting platforms have become the standard for Singapore SMEs precisely because they reduce human error and integrate directly with IRAS filing requirements.

The most widely adopted platforms include Xero, QuickBooks Online, and Zoho Books. QuickBooks Online has surpassed 4.5 million subscribers globally as of 2026, a figure that reflects how decisively the market has moved toward software-driven bookkeeping. Xero is particularly popular among Singapore businesses due to its local bank feed integrations and GST reporting features built for local regulatory requirements.

The practical benefits of using bookkeeping software include:

- Automated bank reconciliation: The software pulls in bank transactions daily, matches them against entries in the ledger, and flags discrepancies. This turns a two-hour manual task into a five-minute review.

- GST filing support: Platforms like Xero generate GST F5 reports directly from transaction data, reducing the risk of miscalculation and saving time during quarterly filing periods.

- Accounts receivable tracking: Automated invoice reminders reduce late payments, which directly improves cash flow without requiring manual follow-up.

- Financial reporting: Profit and loss statements, balance sheets, and cash flow reports can be generated instantly, giving business owners real-time visibility into financial health.

- Multi-user access: Business owners, bookkeepers, and accountants can all access the same data simultaneously, eliminating version control problems associated with shared spreadsheets.

Pro Tip: Do not select bookkeeping software based on price alone. Prioritize platforms that support IRAS GST filing formats and local bank integrations. Switching software mid-year is disruptive and carries a real risk of data migration errors.

Software does not replace the judgment and discipline that good bookkeeping requires. Transactions must still be categorized correctly, invoices must be matched to payments, and unusual entries must be investigated. The technology accelerates the process; the human element maintains its accuracy. For guidance on step-by-step bookkeeping for SMEs, pairing software with a clear workflow is always more effective than relying on either alone.

Common bookkeeping mistakes to avoid

The most frequent bookkeeping problems small business owners encounter are not complex. They are straightforward errors that compound quietly over months until they create a serious compliance or financial problem.

Knowing the patterns helps. Here are the four mistakes that appear most consistently:

- Losing source documents: A missing invoice or receipt creates a gap in the audit trail. Audit trail clarity is the highest risk area for small businesses, because transactions that cannot be traced can be disallowed during IRAS reviews, resulting in tax adjustments and penalties.

- Delayed transaction recording: Entering transactions weekly or monthly rather than daily creates inaccuracies and makes reconciliation difficult. By the time a business owner catches a discrepancy from three weeks ago, tracing it back to the source document takes significantly more time than it would have originally.

- Mixing personal and business finances: Using a single bank account for personal and business transactions is one of the most common errors among early-stage founders. It makes bookkeeping far more complicated and can raise red flags during audits. A dedicated business account is not optional — it is a basic governance requirement.

- Incorrect GST treatment: Claiming GST on non-claimable expenses, or failing to charge output GST on taxable supplies, creates mismatches between books and IRAS filings. These mismatches attract scrutiny and often result in penalties and interest charges.

Recording transactions daily, reconciling monthly, and maintaining organized storage of receipts and documents are the habits that protect a business against these issues. The discipline required is modest. The consequences of ignoring it are not.

For a structured reference on avoiding these errors, the accounting checklist for Singapore businesses covers the most critical tasks by month, quarter, and year end.

How bookkeeping data drives better decisions

Bookkeeping for small businesses is not only a compliance function. The data it generates, when maintained accurately and reviewed regularly, becomes one of the most reliable tools a business owner has for making sound financial and strategic decisions.

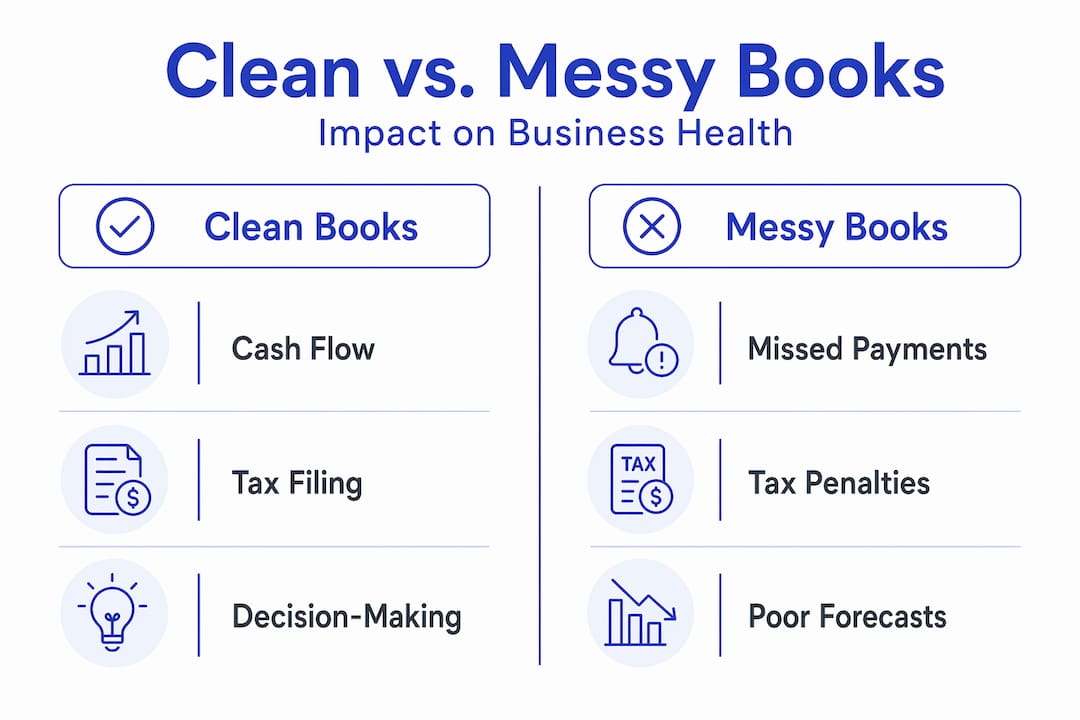

Consider the difference between two businesses at the same revenue level:

| Area | Business with clean books | Business with disorganized books |

|---|---|---|

| Cash flow visibility | Knows exactly what is owed and when payments are due | Regularly surprised by cash shortfalls |

| Tax filing | Submits accurate returns on time with supporting documents | Scrambles at deadline with incomplete records |

| Loan or investment readiness | Can produce audited financials on short notice | Cannot demonstrate financial health to lenders |

| Expense control | Identifies cost overruns monthly and adjusts spending | Discovers overspending only at year end |

| Growth planning | Uses profit trends to time hiring and expansion | Makes growth decisions without financial data |

Accurate bookkeeping protects cash flow and reduces surprises by tracking income and expenses every month. That monthly visibility is what allows a business to set aside funds for tax obligations, spot declining margins before they become serious, and recognize which revenue streams are actually profitable.

Cash flow forecasting, in particular, depends entirely on the accuracy of historical bookkeeping records. A business that reconciles its accounts monthly and maintains complete records can project its cash position three to six months forward with reasonable confidence. One that does not reconcile cannot forecast at all.

Bookkeeping also connects directly to IRAS tax compliance and corporate filing obligations. Accurate books mean accurate tax returns. Accurate tax returns mean no penalties, no unexpected assessments, and no back-and-forth with IRAS auditors over missing documentation. The connection between daily bookkeeping habits and annual tax outcomes is direct and measurable.

For businesses thinking about how bookkeeping fits into broader cash flow management, the short answer is this: bookkeeping is where that management begins. Every decision about when to pay suppliers, when to collect from customers, and how much to set aside for taxes starts with what the books say.

How Bizsquare supports your bookkeeping needs

Managing bookkeeping in-house while running a business is demanding work, and the cost of errors goes beyond time. For Singapore entrepreneurs and SMEs looking to get their books in order without the overhead of a full-time finance hire, Bizsquare offers professional accounting and bookkeeping services designed specifically for the local compliance environment.

The team at Bizsquare manages transaction recording, GST reporting, bank reconciliation, and financial statement preparation using cloud-based platforms aligned with IRAS requirements. Clients receive accurate monthly reports and stay current with all regulatory obligations without diverting management attention from core business operations. For business owners who are still evaluating their options, the guide on DIY vs. professional bookkeeping in Singapore provides a practical framework for making the right choice based on business size, transaction volume, and compliance complexity. If you are weighing whether to keep bookkeeping internal or bring in specialist support, in-house versus outsourced bookkeeping is worth reviewing before committing to either model.

FAQ

What is the bookkeeping definition in simple terms?

Bookkeeping is the systematic recording and organizing of all financial transactions a business makes, including sales, purchases, payments, and receipts. It forms the foundation from which financial statements and tax filings are prepared.

How is bookkeeping different from accounting?

Bookkeeping records raw financial data daily; accounting analyzes that data to produce reports, financial strategies, and tax advice. Bookkeeping is the input; accounting is the interpretation.

What are the main types of bookkeeping systems?

The two primary types of bookkeeping systems are single-entry and double-entry. Single-entry records each transaction once and suits very simple businesses. Double-entry records every transaction as both a debit and a credit, providing greater accuracy and is required for companies that must produce formal financial statements in Singapore.

How long must Singapore companies keep bookkeeping records?

Singapore law requires companies to retain all accounting records and source documents for a minimum of seven years under Companies Act Section 199, with GST-related documents subject to a five-year retention requirement under IRAS guidelines.

What is bookkeeping software and do small businesses need it?

Bookkeeping software automates the recording, categorization, and reconciliation of financial transactions. Platforms like Xero, QuickBooks, and Zoho Books integrate with local bank feeds and support GST filing, making them highly practical for Singapore small businesses that want accuracy without excessive manual work.