Master Business Tax Computation in Singapore: Step-by-Step

Miscalculating corporate tax or overlooking available exemptions can cost Singapore SMEs thousands of dollars annually, whether through unnecessary tax payments or penalties from IRAS. The corporate tax computation process starts with net profit or loss from financial statements, applies specific adjustments, and arrives at chargeable income taxed at a flat 17% rate. For business owners and financial managers, understanding each step is not merely a compliance exercise. It is a genuine opportunity to protect cash flow, claim legitimate savings, and reduce audit exposure. This guide covers the full process: framework, preparation, step-by-step calculation, filing procedures, and verification.

Table of Contents

- Understanding the corporate tax framework in Singapore

- Preparing your records: What you need before computation

- Step-by-step computation process: From net profit to chargeable income

- Filing procedures, deadlines, and verification tools

- Expert perspective: Why strategic tax computation is more than compliance

- Connect with trusted advisors for your tax needs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Start from net profit | Begin computation with your company’s net profit and apply IRAS-required adjustments step-by-step. |

| Use SME exemptions | Partial and Start-Up Tax Exemptions significantly lower effective tax rates and save money. |

| Prepare documents early | Gather all records and receipts ahead of time to minimize errors and ensure compliance. |

| Follow filing deadlines | Submit ECI within 3 months and Form C-S/Lite/C by November 30 to avoid penalties. |

| Leverage IRAS tools | Download IRAS calculators and checklists to validate your tax computation and prevent mistakes. |

Understanding the corporate tax framework in Singapore

Singapore operates on a territorial basis for corporate taxation, meaning only income accrued in or derived from Singapore, or received in Singapore from abroad, is subject to tax. This principle matters because it directly shapes which revenue streams you include in your computation and which you may legitimately exclude.

The headline corporate tax rate is 17%, but this figure rarely reflects what SMEs actually pay after exemptions. Taxable income comprises gains and profits from trade or business, as well as investment income such as dividends, interest, and rental income accrued or derived in Singapore. Capital gains are generally non-taxable unless the gains are characterized as trading income based on the nature of transactions.

For SMEs, two exemption schemes significantly reduce the effective tax rate:

- Start-Up Tax Exemption (SUTE): Available to qualifying new companies for the first three consecutive years of assessment. It provides 75% exemption on the first S$100,000 of chargeable income and 50% on the next S$100,000.

- Partial Tax Exemption (PTE): Available to all other companies. The PTE scheme provides 75% exemption on the first S$10,000 of chargeable income and 50% exemption on the next S$190,000.

The table below illustrates the impact of PTE on a company with S$200,000 chargeable income:

| Chargeable income | Exemption rate | Exempt amount | Taxable amount |

|---|---|---|---|

| First S$10,000 | 75% | S$7,500 | S$2,500 |

| Next S$190,000 | 50% | S$95,000 | S$95,000 |

| Total | S$102,500 | S$97,500 |

At 17%, the tax payable on S$97,500 is approximately S$16,575, compared to S$34,000 without any exemption. That difference is real money that stays in your business. Understanding filing corporate tax in Singapore starts with knowing these exemptions cold. For a broader overview of rates and policies, the corporate tax in Singapore guide provides useful context.

Preparing your records: What you need before computation

With the framework clear, it is important to lay the groundwork for a successful computation. Errors in tax computation rarely stem from misunderstanding the rules. They most often arise from incomplete or disorganized records. IRAS emphasizes that accurate adjustments are vital to avoid common errors like omitting income or claiming wrong deductions, and companies must retain records for at least five years.

Before you begin any calculation, gather the following documents:

- Audited or unaudited financial statements for the relevant financial year

- General ledger and trial balance to verify individual account balances

- Invoices and receipts for all revenue and expense items

- Fixed asset register for capital allowance claims

- Donation receipts from approved institutions of a public character (IPCs)

- Prior year tax returns and notices of assessment for reference

- Loan agreements and interest schedules if interest deductions are claimed

- Tenancy agreements if rental income or expense is involved

The complexity of preparation varies significantly depending on your company’s structure. The table below contrasts two common scenarios:

| Factor | Standard trading SME | Investment holding company (IHC) |

|---|---|---|

| Primary income source | Business profits | Dividends, interest, rental |

| Key adjustments | Disallowable expenses, capital allowances | Expense apportionment, group concessions |

| Record complexity | Moderate | High |

| Audit risk | Lower | Higher without meticulous tracking |

For companies with investment income, expense apportionment between taxable and non-taxable income is a particularly sensitive area. Getting this wrong is one of the fastest routes to a IRAS query or audit.

Pro Tip: IRAS provides a structured tax computation template as part of its guidance materials. Using this template as your working document ensures you follow the correct sequence of adjustments and reduces the chance of omitting a required step. Your corporate tax filing advisory provider can also supply a customized checklist aligned to your specific business structure.

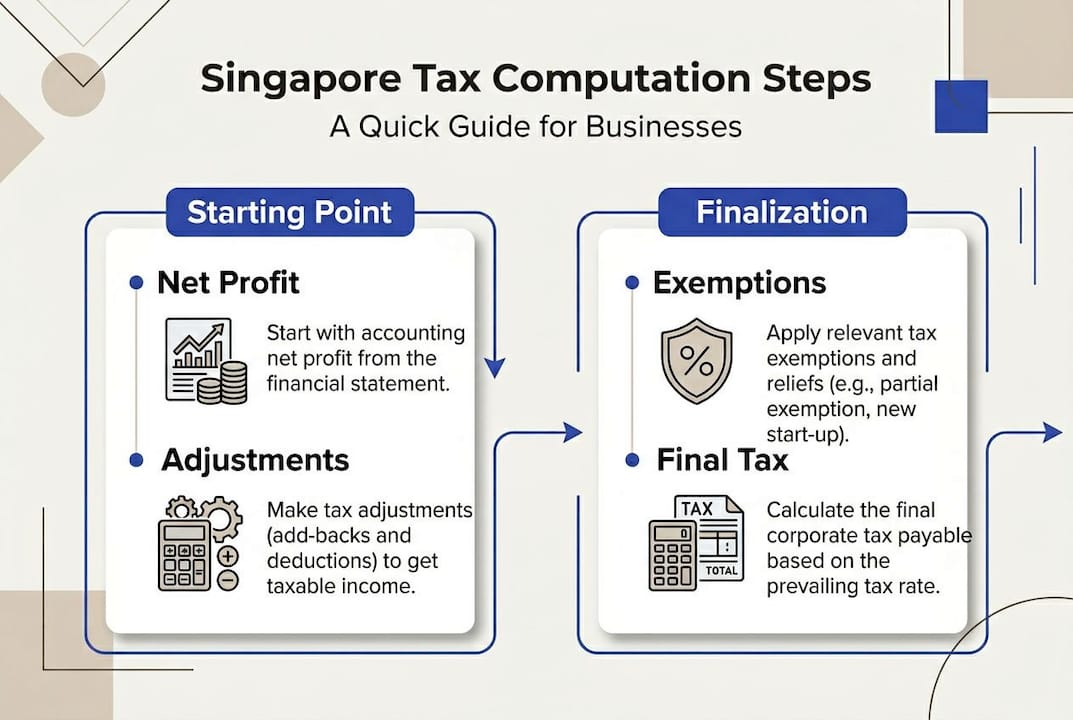

Step-by-step computation process: From net profit to chargeable income

Once documents are ready, you can follow this computation process. The goal is to move from the accounting net profit figure in your financial statements to the chargeable income figure that IRAS will tax. These two numbers are almost never the same.

Here is the standard sequence of adjustments:

- Start with net profit (or loss) as reported in the financial statements.

- Deduct non-taxable income, such as capital gains or exempt dividends, which were included in accounting profit but are not subject to tax.

- Deduct investment income assessed separately, since items like rental income may be computed under a different schedule.

- Add back disallowable expenses, meaning costs that were deducted in the accounts but are not tax-deductible. Examples include private motor vehicle expenses, penalties, and non-business entertainment.

- Add direct expenses related to investment income that were deducted in the profit and loss account.

- Deduct Section 14N renovation and refurbishment expenses, which qualify for a three-year write-off under specific conditions.

- Deduct capital allowances on qualifying plant and machinery.

- Deduct approved donations at 2.5 times the donated amount. Note that donations must first be added back as non-deductible in step 4, then deducted at 2.5x for qualifying approved donations, a provision currently extended until 2029. Pre-commencement expenses are also deductible if incurred within one year prior to the first revenue receipt.

- Apply tax exemptions (PTE or SUTE) to arrive at net chargeable income.

- Multiply by 17% to calculate tax payable before rebates.

The key adjustments outlined by IRAS follow this exact logic, and each line requires documentary support. For YA2025 and YA2026, additional corporate income tax rebates of 50% (capped at S$40,000) plus a S$2,000 cash grant for companies with local employees further reduce the final liability. Stay current with SME tax updates to capture these rebates accurately.

Pro Tip: Work through the computation in a structured spreadsheet with clearly labeled rows for each adjustment. This systematic approach not only reduces errors but also creates an audit trail that demonstrates good governance if IRAS ever requests supporting documents. Review the full tax filing steps to understand how your computation feeds into the final submission.

Filing procedures, deadlines, and verification tools

With your computation finalized, filing and verification ensure compliance. Even a perfectly prepared computation loses its value if it is filed incorrectly or after the deadline.

Singapore companies must meet two key filing obligations:

- Estimated Chargeable Income (ECI): Must be filed within three months of the financial year end. ECI is an estimate of your chargeable income for the year.

- Form C-S, Form C-S (Lite), or Form C: Must be filed by November 30 of the relevant Year of Assessment (YA). The appropriate form depends on company revenue and complexity.

| Filing form | Who it applies to | Revenue threshold |

|---|---|---|

| Form C-S (Lite) | Straightforward companies | S$200,000 or below |

| Form C-S | Qualifying companies | S$5 million or below |

| Form C | All other companies | Above S$5 million |

IRAS provides a Basic Corporate Income Tax Calculator in Excel format with built-in validation, available for YA2025 and beyond. This tool is particularly useful for SMEs computing tax without dedicated tax software. It covers standard formats as well as specialized formats for investment holding companies and shipping companies.

Common errors that trigger IRAS queries include:

- Omitting income streams, particularly foreign-sourced income received in Singapore

- Claiming deductions for expenses that are capital in nature

- Failing to apportion expenses between taxable and non-taxable income

- Late filing, which results in estimated assessments and potential penalties

“Over-reliance on accounting profit without proper tax adjustments is one of the most common and costly mistakes SMEs make. The gap between book profit and chargeable income can be significant, and ignoring it creates real financial risk.”

For companies seeking to verify their IRAS tax compliance posture, IRAS also publishes detailed checklists for each form type. If your company qualifies for SUTE, reviewing the startup exemption guide before filing is strongly recommended to ensure all conditions are met.

Expert perspective: Why strategic tax computation is more than compliance

Most financial managers approach tax computation as an annual obligation to be completed and filed. That framing leaves money on the table. Tax computation, done well, functions as a structured annual review of your company’s financial decisions and their tax consequences.

Consider this: most SMEs that miss PTE or SUTE claims do so not because they are ineligible, but because their records are incomplete or their adjustments are rushed. The exemption is available, but the documentation is not there to support it. That is a recoverable problem with better processes, not a tax law problem.

For investment holding companies, the stakes are even higher. Foreign-sourced income is exempt only if it has been taxed abroad at a rate of at least 15% and the exemption is beneficial to the company. Tracking this meticulously is non-negotiable. IHCs also face strict expense apportionment rules under group and block concessions for dividends and rental income. Errors here invite audits.

The strategic angle is this: treat your tax computation as a diagnostic tool. Review which expense categories are being added back repeatedly. Those are signals of either policy misalignment or record-keeping gaps that cost you deductions year after year. Monitor budget updates for SMEs as new reliefs and rebates are introduced regularly and can meaningfully shift your effective rate.

Pro Tip: Schedule your tax computation review at least six weeks before the filing deadline. This gives you time to identify missing documentation, consult advisors, and make corrections without the pressure of an imminent due date.

Connect with trusted advisors for your tax needs

Navigating Singapore’s corporate tax computation process with precision requires both technical knowledge and organized financial records. Whether you are preparing your first computation or refining an existing process, having the right guidance makes a measurable difference in outcomes.

Bizsquare Accounting’s consultants specialize in corporate tax computation and advisory for SMEs across Singapore. From reviewing your adjustment schedules to ensuring you capture every available exemption, our team provides the accuracy and strategic insight your business needs. Explore our detailed corporate tax filing guide for step-by-step reference, or connect directly with our tax advisory services team for tailored support aligned to your company’s structure and financial year.

Frequently asked questions

What is the corporate tax rate in Singapore and how is it applied?

Singapore’s corporate tax rate is 17%, applied on net chargeable income after all required adjustments and applicable exemptions have been factored in. The effective rate for most SMEs is considerably lower once PTE or SUTE is applied.

How do Partial Tax Exemption (PTE) and Start-Up Tax Exemption (SUTE) benefit SMEs?

PTE and SUTE reduce the effective tax rate by exempting a significant portion of chargeable income, allowing SMEs and qualifying startups to retain more capital for reinvestment and operations.

Which business expenses can be deducted during tax computation?

Deductible expenses include those wholly and exclusively incurred for business purposes, capital allowances and approved donations at 2.5 times the donated amount, and pre-commencement expenses incurred within one year before the first revenue receipt.

What are common mistakes in tax computation for SMEs?

Omitting income or claiming wrong deductions are the most frequent errors, alongside failing to apply available exemptions, all of which can trigger IRAS queries, penalties, or formal audits.

What’s the deadline for filing corporate tax in Singapore?

ECI must be filed within three months of the financial year end, while Form C-S, Form C-S (Lite), or Form C must be submitted by November 30 of the relevant Year of Assessment.