The Role of Management Accounts in Business Decision Making

Overview

Management accounts provide internal financial insights that guide decision-making for Singapore SMEs. They are produced monthly or quarterly, offering real-time information that helps prevent problems and supports growth. Regularly reconciling accounts and analyzing variances enables businesses to make timely strategic choices and improve financial control.

Management accounts are defined as internal financial reports that give business owners and financial managers timely insight into performance, cash flow, and costs. Unlike statutory accounts filed with regulators, management accounts exist purely to guide decisions inside the business. The role of management accounts is to close the gap between raw financial data and the strategic choices that drive growth. For Singapore SMEs and growing companies, this distinction is not academic. It is the difference between reacting to problems after the fact and preventing them before they escalate.

What is the role of management accounts in business?

Management accounts serve as the internal compass of a business. They translate financial data into clear signals about what is working, what is not, and where attention is needed. The Institute of Management Accountants defines management accounting as a profession that involves partnering in management decision-making and performance management systems. That definition places management accounts at the center of business strategy, not just at the edge of compliance.

The core functions of management accounting include budgeting, forecasting, variance analysis, cost control, and cash flow monitoring. Each function answers a specific business question. Budgeting answers “what do we plan to spend?” Variance analysis answers “why did actual results differ from the plan?” Cash flow monitoring answers “do we have enough money to operate next month?” Together, these functions give business owners a complete picture of financial health at any point in time.

For Singapore businesses operating in a fast-moving market, the importance of management accounts grows with the size and complexity of the company. Fast-growing SMEs treat management accounts as non-optional navigational tools once turnover reaches a meaningful scale. The reports become the foundation for every major decision, from hiring to capital investment.

How do management accounts differ from statutory financial accounts?

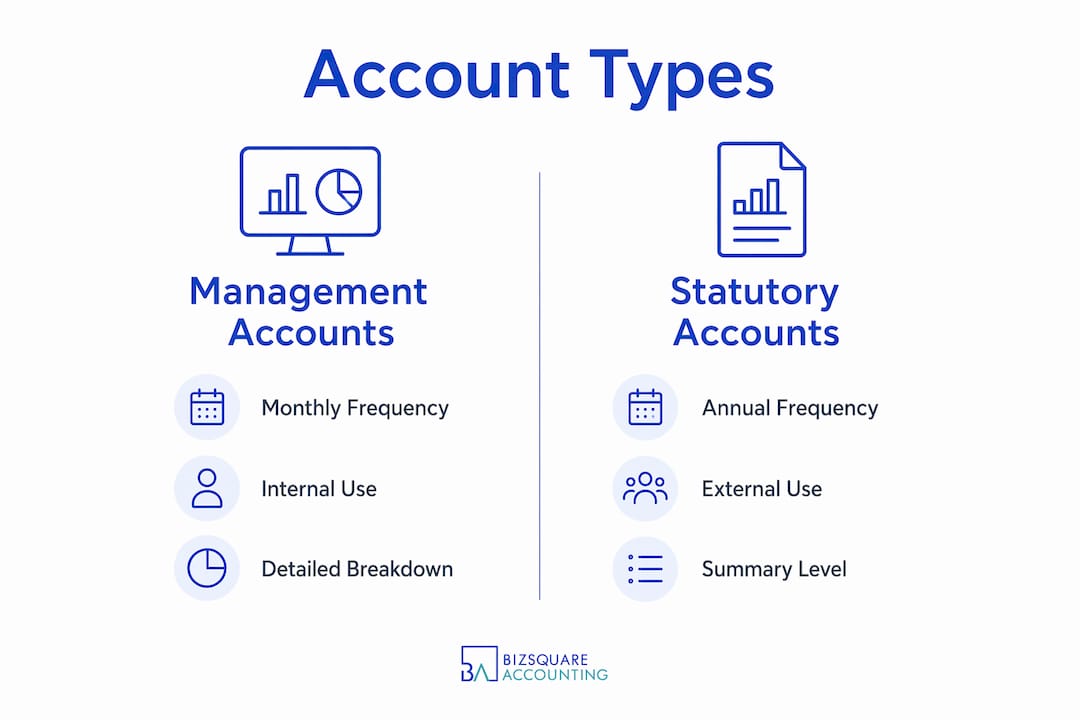

The most important distinction is timing. Management accounts are produced monthly or quarterly, giving business owners insights within weeks of the reporting period. Statutory accounts, by contrast, can be 9–18 months old by the time they are filed with regulators. That lag makes statutory accounts unsuitable for real-time decisions.

The purpose also differs fundamentally. Management accounts are prepared for internal use. They help directors and managers run the business day to day. Statutory accounts are prepared for external stakeholders, including the Accounting and Corporate Regulatory Authority (ACRA) in Singapore, tax authorities like the Inland Revenue Authority of Singapore (IRAS), and shareholders. Statutory accounts must follow Singapore Financial Reporting Standards (SFRS). Management accounts follow no mandatory format, which gives businesses the flexibility to design reports that match their specific needs.

The level of detail is another key difference. Management accounts can break down revenue and costs by product line, department, project, or customer segment. Statutory accounts aggregate this data into standardized categories. A business owner reading statutory accounts sees the total picture. A business owner reading management accounts sees exactly which product is underperforming or which department is overspending.

The table below summarizes the key differences:

| Feature | Management accounts | Statutory accounts |

|---|---|---|

| Frequency | Monthly or quarterly | Annually |

| Purpose | Internal decision-making | External compliance and legal filing |

| Format | Flexible, tailored to business needs | Standardized under SFRS |

| Audience | Directors, managers, internal teams | ACRA, IRAS, shareholders, auditors |

| Level of detail | Granular, by product or department | Aggregated, high-level |

| Timeliness | Within weeks of period end | 9–18 months after period end |

Both types of accounts must align. Management accounts must reconcile to statutory accounts to prevent audit and tax reconciliation issues. A significant gap between the two signals weak internal controls, which creates risk during audits and tax reviews. Businesses that maintain bookkeeping accuracy throughout the year find this reconciliation far easier to manage.

What are the primary functions and benefits of management accounts?

The benefits of management accounts extend well beyond basic financial reporting. Each function addresses a specific operational or strategic need.

Financial planning and budgeting

Management accounts form the foundation of any reliable budget. They provide actual historical data that makes forward projections realistic rather than speculative. A business that reviews management accounts monthly can update its annual budget based on real performance, not assumptions made twelve months earlier.

Variance analysis

Variance analysis is a core management accounting technique where managers investigate differences between budgeted and actual costs. A 20% labor cost overshoot, for example, must be analyzed to determine whether it reflects a one-time event or a structural problem. Without this analysis, the overshoot simply repeats. With it, the business can take corrective action before the variance compounds.

Pro Tip: Set a materiality threshold for variance analysis. Investigate any variance that exceeds 10% of the budgeted line item or SGD 5,000, whichever is lower. This keeps analysis focused on what actually matters.

Cash flow management

Profit on paper does not guarantee solvency. Management accounts highlight the difference between profit and actual cash flow, revealing risks from slow-paying receivables or timing mismatches that could cause insolvency despite a profitable income statement. A Singapore business showing strong net profit can still run out of cash if customers pay late and suppliers demand early payment. Management accounts make this risk visible before it becomes a crisis.

KPI and departmental reporting

The best management accounts pack is one that directors actually read and act upon, built around granular, department-level data rather than aggregated totals. Key performance indicators (KPIs) tied to specific business goals, such as gross margin by product, revenue per salesperson, or cost per acquisition, give managers the specific signals they need to act. Generic totals do not.

Cost control and efficiency

Management accounts reveal where costs are growing faster than revenue. This visibility allows management to identify inefficiencies, renegotiate supplier contracts, or restructure operations before margins erode. Without regular reporting, cost creep goes unnoticed until it appears in the annual statutory accounts, by which point the damage is done.

Tax planning support

Management accounting aids in tax planning by providing foundational financial insight long before statutory compliance deadlines. Businesses that track income and expenses monthly can make informed decisions about capital expenditure timing, director remuneration, and deductible costs well ahead of the IRAS filing deadline.

How can Singapore businesses use management accounts for decision-making?

Producing management accounts is only half the work. The other half is using them consistently and correctly. Here is a practical approach for Singapore business owners and financial managers.

- Review management accounts at every board or leadership meeting. Schedule a fixed agenda item for financial review. This creates accountability and ensures that decisions are grounded in current data rather than intuition.

- Use reports to inform investment decisions. Before approving a new hire, a capital purchase, or a market expansion, review the relevant cost center or product line performance in the management accounts. The data will confirm whether the business can afford the investment and whether the expected return is realistic.

- Set pricing based on actual cost data. Many Singapore SMEs price products based on market rates without knowing their true cost of delivery. Management accounts reporting at the product or service level reveals actual margins, which allows pricing decisions that protect profitability.

- Monitor cash flow weekly, not just monthly. Management accounts typically cover a monthly period, but cash flow can shift within weeks. Use the cash flow statement in your management accounts as a baseline, then track actual bank balances weekly against the projected position.

- Act on variances within the same reporting period. A variance identified in the january management accounts should trigger a corrective action by february. Waiting until the next quarter review allows the problem to compound.

Pro Tip: Avoid the common mistake of treating management accounts as a backward-looking report. The most valuable use of management accounts in decision-making is forward projection. Use the current period actuals to reforecast the next three months every time you review.

One of the most common pitfalls in management accounts reporting is confusing profit with cash flow. Business owners often confuse profit and cash flow, and management accounts explicitly reveal timing issues that can threaten solvency despite showing profits. A business owner who sees a profitable income statement but ignores the cash flow statement is reading only half the story. Both statements must be reviewed together at every reporting cycle.

For practical guidance on accounting services in Singapore, understanding how management accounts fit within the broader financial reporting structure helps businesses build a more complete financial management system.

What are the challenges and best practices in producing reliable management accounts?

Producing reliable management accounts consistently is harder than it looks. Several common challenges undermine the quality and usefulness of these reports.

- Reconciliation gaps. Management accounts that do not reconcile to statutory accounts create serious problems at year-end. Regular reconciliation with statutory accounts prevents tax and audit complications. Businesses should reconcile at least quarterly, not just at year-end.

- Data quality issues. Management accounts are only as reliable as the underlying bookkeeping. Incomplete transaction records, misclassified expenses, or delayed invoice processing all distort the reports. Strong bookkeeping practices are the foundation of accurate management accounts.

- Report complexity without clarity. A management accounts pack that runs to forty pages with no executive summary serves no one. Reports should be concise, relevant, and tailored to what the reader needs to decide. Actionable management accounts are tailored, relevant, and concise, avoiding the trap of overwhelming management with unnecessary data.

- Delayed production. Management accounts produced six weeks after the period end are far less useful than those produced within two weeks. Businesses should set a firm close schedule and hold the finance team accountable to it.

- Gaps between data and strategic action. Failures in realizing management accounts’ value arise primarily from the inability to interpret data and apply it strategically, not from technology limitations. A business can have excellent reports and still make poor decisions if no one with financial expertise is guiding the interpretation.

Best practices to address these challenges include the following:

- Assign a named owner for management accounts production and review.

- Use a consistent chart of accounts that mirrors the statutory accounts structure.

- Build a monthly close checklist that covers bank reconciliation, accruals, and prepayments.

- Engage a finance professional, such as an outsourced CFO or senior accountant, to interpret results and recommend actions.

- Review the management accounts format annually to confirm it still reflects the business’s current priorities.

Internal control systems also play a direct role in reliability. Segregation of duties, approval workflows for expenses, and regular bank reconciliations all reduce the risk of errors entering the management accounts. For Singapore businesses subject to IRAS scrutiny, IRAS tax compliance is significantly easier when management accounts are accurate and well-maintained throughout the year.

Key Takeaways

Management accounts are the primary tool for internal financial control, and their value depends entirely on the quality of the data, the frequency of review, and the quality of interpretation applied to the results.

| Point | Details |

|---|---|

| Timing advantage | Management accounts deliver insights within weeks, while statutory accounts lag by 9–18 months. |

| Cash flow visibility | Profit figures alone do not reveal solvency risk; management accounts show cash timing gaps that could threaten operations. |

| Variance analysis | Investigating budget-versus-actual differences monthly allows corrective action before variances compound. |

| Reconciliation discipline | Management accounts must reconcile to statutory accounts to avoid audit and tax complications at year-end. |

| Finance leadership | Technology does not unlock the value of management accounts; skilled financial interpretation does. |

Management accounts as a strategic tool, not just a report

Management accounting is more than a static report. It is a process intertwined with strategic finance leadership and organizational planning. After working with Singapore SMEs across multiple industries, one pattern stands out clearly. The businesses that use management accounts well do not treat them as a compliance exercise. They treat them as a live conversation between the numbers and the strategy.

The most common mistake I see is producing excellent reports that no one acts on. The finance team delivers a clean pack every month. The directors glance at the bottom line. Then nothing changes. That gap between data and decision is not a technology problem. It is a leadership problem. The business needs someone in the room who can translate “your gross margin dropped 3% this quarter” into “here is why, and here is what we do about it.”

Singapore’s business environment in 2026 moves quickly. Interest rates, supply chain costs, and labor markets shift faster than annual statutory accounts can capture. Management accounts reporting on a monthly cycle gives business owners the frequency they need to stay ahead of these shifts. Businesses that rely solely on annual statutory accounts are, in effect, driving by looking in the rearview mirror.

The other insight worth emphasizing is the profit-versus-cash-flow trap. Many profitable Singapore businesses have faced serious cash flow pressure because receivables stretched out while payables came due. Management accounts make this risk visible in real time. No business should be surprised by a cash shortfall that was predictable three months earlier.

How Bizsquare helps Singapore businesses get more from management accounts

Bizsquare provides accounting, bookkeeping, and outsourced CFO services designed specifically for Singapore SMEs and growing companies. The team goes beyond transaction recording to deliver management accounts that are timely, reconciled, and built for decision-making.

For business owners who want financial reports that actually drive decisions, Bizsquare’s management consulting services offer the finance leadership layer that turns numbers into strategy. The team handles everything from monthly close processes to variance analysis and cash flow forecasting, so business owners can focus on running the company. Contact Bizsquare to discuss how professional management accounting support can strengthen your financial position in 2026.

FAQ

1.) What is the role of management accounts?

Management accounts are internal financial reports that give business owners and managers timely insight into performance, cash flow, and costs. Their primary role is to support informed decision-making inside the business, not to satisfy external regulatory requirements.

2.) How often should management accounts be prepared?

Management accounts are typically prepared monthly or quarterly. Monthly preparation gives the most current view and allows faster corrective action when performance deviates from plan.

3.) What is the difference between management accounts and statutory accounts?

Management accounts are internal, flexible, and produced frequently for decision-making. Statutory accounts are external, standardized under SFRS, and filed annually with ACRA and IRAS, often 9–18 months after the reporting period.

4.) Why do management accounts matter for cash flow management?

Profit on the income statement does not guarantee cash in the bank. Management accounts reveal timing gaps between income and expenses that can cause insolvency even when the business appears profitable on paper.

5.) What happens if management accounts do not reconcile with statutory accounts?

A failure to reconcile signals weak internal controls and creates complications during tax reviews and audits by IRAS. Regular reconciliation, at least quarterly, prevents these issues from accumulating at year-end.

6.) Who should review management accounts in a Singapore business?

Directors, financial managers, and any senior leader responsible for budget decisions should review management accounts at every leadership meeting. An outsourced CFO or senior accountant should guide the interpretation and recommend actions.

7.) Can management accounts help with IRAS tax planning?

Management accounts provide detailed financial data throughout the year, which allows businesses to make informed decisions about capital expenditure, director remuneration, and deductible costs well before the IRAS filing deadline.

8.) What should a good management accounts pack include?

A reliable management accounts pack includes a profit and loss statement, balance sheet, cash flow statement, variance analysis against budget, and KPI summaries by department or product line.

9.) How do management accounts support business growth in Singapore?

Management accounts give business owners the financial visibility to identify which products, services, or departments are driving growth and which are dragging performance. This clarity supports confident investment and expansion decisions.

10.) What are the most common mistakes in management accounts reporting?

The most common mistakes are confusing profit with cash flow, producing reports too late to act on, and failing to investigate variances before the next reporting period. A second common error is producing detailed reports without a finance professional to interpret and apply the findings.