Accounting Standards in Singapore: 2026 Guide

Overview

Singapore’s accounting standards align closely with international norms, with local adaptations vital for compliance. The dual framework—SFRS and SFRS(I)—serves different entities, requiring careful application to avoid costly errors. Staying updated and properly documenting eligibility thresholds ensure firms meet regulatory and international reporting requirements effectively.

Singapore’s accounting standards sit closer to international norms than most practitioners realize, yet the local adaptations matter enormously for compliance. Accounting standards in Singapore operate under a dual framework: Singapore Financial Reporting Standards (SFRS) and SFRS(I), the internationally aligned variant. Choosing between them, staying current with regulatory updates, and correctly applying the eligibility thresholds for simplified reporting are where most businesses and accountants make costly errors. This guide covers every framework, every key regulator, and every critical update affecting financial reporting in Singapore through 2026 and beyond.

Table of Contents

- Key Takeaways

- Accounting standards in Singapore: the core frameworks

- Regulatory compliance and enforcement in Singapore

- SFRS vs. SFRS for Small Entities: practical considerations

- Recent and upcoming updates to Singapore’s standards

- Why accounting standards deserve more than compliance-driven attention

- How Bizsquareaccounting helps you stay compliant

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Dual framework structure | Singapore operates SFRS and SFRS(I) concurrently, with each serving distinct entity types and capital market needs. |

| SME eligibility thresholds | Qualifying for simplified SFRS for Small Entities requires meeting two of three criteria: revenue, assets, or employee count. |

| ASC and ACRA authority | The Accounting Standards Council sets the standards; ACRA enforces them with legal authority under the Companies Act. |

| IFRS alignment is strategic | Adopting SFRS(I) signals international credibility and opens access to global capital markets. |

| 2027 amendment incoming | ACRA’s update to SFRS(I) 1-21 and FRS 21 for hyperinflationary currencies takes effect January 1, 2027. |

Accounting standards in Singapore: the core frameworks

Understanding which framework applies to a given entity is the foundation of accounting compliance Singapore practitioners must get right before preparing a single journal entry. Singapore currently operates three primary reporting frameworks, and each exists for a specific purpose.

Singapore Financial Reporting Standards (SFRS) is the primary framework for domestic companies not listed on the Singapore Exchange (SGX). The Accounting Standards Council (ASC) serves as Singapore’s primary authority for setting SFRS and SFRS(I) under the Accounting Standards Act 2007, and it works to align these standards with IFRS while adapting them to local regulatory conditions. This is a critical point many professionals overlook: SFRS is not simply IFRS copied verbatim. There are deliberate local adjustments, and applying IFRS interpretations directly without referencing the Singapore-specific text creates compliance risk.

SFRS(I) carries the “International” suffix for a reason. It is designed for entities that require or seek comparability with international financial statements, particularly SGX-listed companies. SFRS(I) 9 is technically identical to IFRS 9, which means full compliance with global standards rather than a local approximation. For Singapore companies seeking capital from overseas investors or cross-listed on foreign exchanges, this alignment functions as a practical passport to international markets.

SFRS for Small Entities offers a simplified reporting path for companies that qualify. The framework removes complex disclosure requirements and reduces the volume of notes required, but it does not abandon foundational accounting principles. The following points summarize what the simplified framework retains and removes:

- Accrual accounting and the fair value principle remain intact under the simplified framework

- Disclosures such as earnings per share and interim reporting requirements are excluded, reducing complexity for SMEs

- Segment reporting and certain financial instrument disclosures are also not required under the simplified approach

- Basic principles of revenue recognition and lease accounting still apply, though with reduced disclosure depth

Beyond these three, practitioners also work with specific Financial Reporting Standards (FRS) that address individual topics such as financial instruments (FRS 109), revenue recognition (FRS 115), leases (FRS 116), and inventories (FRS 2). These standards operate within the SFRS ecosystem and are updated in parallel with their IFRS equivalents.

Singapore’s dual-framework approach balances global alignment with the practical need to reduce reporting burdens on smaller firms. The design is intentional and logical once you understand its purpose.

Regulatory compliance and enforcement in Singapore

Knowing the frameworks is only half the obligation. The other half is understanding who enforces them and what the consequences of non-compliance look like. Several bodies govern Singapore financial regulations, each with a distinct mandate.

- Accounting Standards Council (ASC): The ASC holds legislative authority under the Accounting Standards Act 2007 to issue and amend SFRS and SFRS(I). Its role is prescriptive. It defines what financial statements must contain, how items must be measured, and what disclosures are required.

- Accounting and Corporate Regulatory Authority (ACRA): ACRA functions as the primary enforcement body for accounting compliance Singapore. It registers companies, reviews filed financial statements, conducts regulatory audits, and investigates breaches. Companies that file materially non-compliant financial statements face formal investigation, and directors can face personal liability under the Companies Act.

- Companies Act: The Companies Act mandates that Singapore-incorporated companies prepare financial statements in accordance with SFRS and submit them annually to ACRA. This is not optional. Even dormant companies have reporting obligations unless formally granted an exemption.

- Singapore Exchange (SGX): Listed companies face an additional regulatory layer. SGX requires adoption of SFRS(I) and mandates specific disclosure practices in annual reports and quarterly announcements. SGX’s Listing Rules incorporate accounting standards compliance as a condition of maintaining a listing.

- Inland Revenue Authority of Singapore (IRAS): While IRAS does not set accounting standards, SFRS financial statements form the basis for corporate tax filings with IRAS. Errors in financial reporting cascade directly into tax computation errors, creating dual exposure to both ACRA and IRAS.

The penalty framework for non-compliance includes fines for late filing, potential director disqualification for persistent offenses, and formal investigations that can result in court proceedings. Most enforcement actions begin with ACRA’s routine review of annual filings, which means quality at the point of submission is the first defense against regulatory attention.

Pro Tip: Review the new ACRA rules for 2026 as part of your annual compliance calendar. Regulatory updates take effect mid-year or at fiscal year start, and missing the effective date on a single amendment can invalidate an entire set of financial statements.

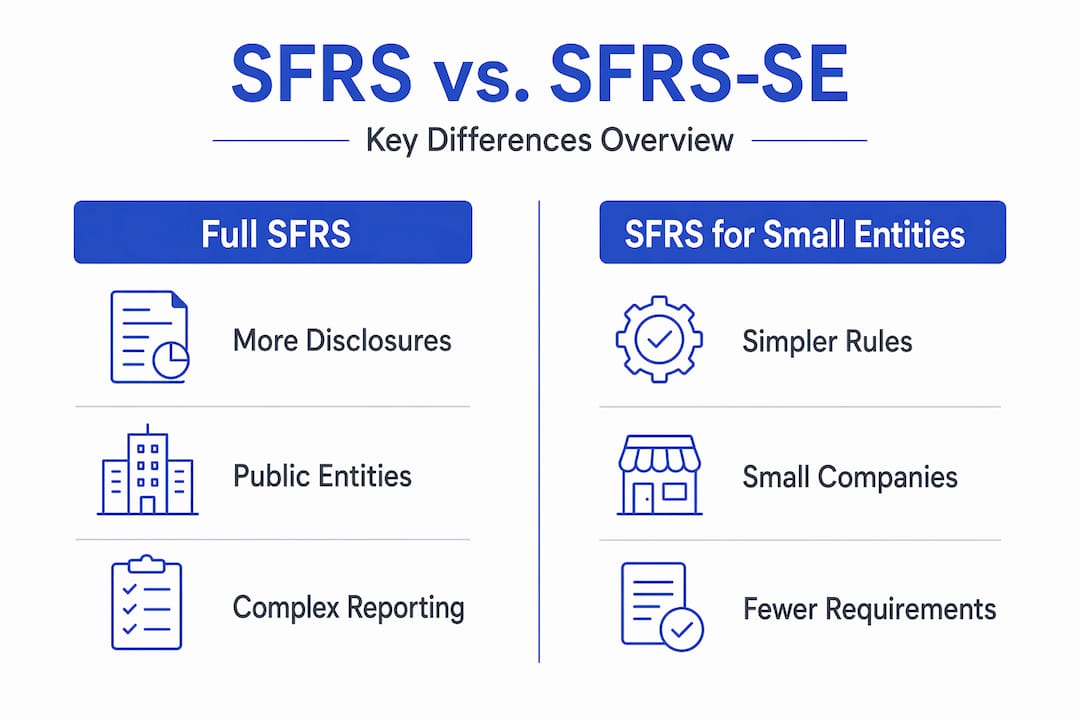

SFRS vs. SFRS for Small Entities: practical considerations

The decision between full SFRS and the simplified framework is not purely a size question. It involves threshold calculations, documentation discipline, and a clear assessment of where the business is headed.

Eligibility thresholds explained

To qualify for SFRS for Small Entities, a company must satisfy at least two of three criteria: total annual revenue not exceeding S$10 million, total gross assets not exceeding S$10 million, or total employees not exceeding 50. Meeting two of these three puts the company in scope for the simplified framework.

The threshold test is assessed annually, which creates a common trap. A company that grows past two thresholds in a given year may lose eligibility and must transition to full SFRS for the following reporting period. Transitioning mid-growth phase, when operational complexity is increasing, adds significant reporting burden at precisely the wrong moment.

Key differences between the two frameworks

| Feature | Full SFRS | SFRS for Small Entities |

|---|---|---|

| Earnings per share disclosure | Required | Not required |

| Segment reporting | Required for listed companies | Not required |

| Interim financial reporting | Required (listed entities) | Not required |

| Financial instrument complexity | Full fair value and hedge accounting | Simplified measurement |

| Cash flow statement | Always required | Required |

| Statement of changes in equity | Required | Required |

| Audit requirement | Mandatory for qualifying companies | Mandatory if criteria met |

The reduction in disclosure requirements under the simplified framework translates directly to lower preparation time and lower professional fees. For a company with fewer than 20 employees and S$3 million in annual revenue, applying full SFRS would mean preparing disclosures that serve no practical purpose for any of its stakeholders.

That said, the simplified framework is not appropriate for every qualifying entity. Companies that plan to seek institutional funding, list on SGX, or establish joint ventures with foreign partners often adopt full SFRS voluntarily. Presenting audited full SFRS statements signals a level of governance maturity that the simplified framework does not convey with the same weight.

Pro Tip: Maintaining comprehensive working papers that document your threshold calculations is critical. Proper eligibility documentation is the first thing auditors request when reviewing SFRS for Small Entities eligibility, and gaps in those records can trigger reclassification disputes.

For practical guidance on staying organized across both frameworks, the accounting best practices for Singapore SMEs resource from Bizsquareaccounting provides a structured approach to tracking eligibility and managing reporting obligations.

Recent and upcoming updates to Singapore’s standards

Singapore’s accounting standards are not static. The Accounting Standards Council updates SFRS and SFRS(I) regularly to mirror amendments issued by the International Accounting Standards Board (IASB), and 2026 and 2027 bring several changes that practitioners must already be incorporating into their planning.

ACRA’s amendment to SFRS(I) 1-21 and FRS 21: The most consequential near-term update addresses hyperinflationary currency translation. ACRA updated SFRS(I) 1-21 and FRS 21 concurrently, with the new rules taking effect from January 1, 2027. Companies reporting in or operating within hyperinflationary economies will be most directly affected. The synchronized update across both SFRS(I) and FRS frameworks is itself significant, as it reduces discrepancies in multi-framework reporting within corporate groups that include entities under different frameworks.

ISCA’s Financial Reporting Taskforce: The Institute of Singapore Chartered Accountants launched a new taskforce specifically to evaluate and improve financial reporting quality. The taskforce aims to enhance financial reporting quality and uphold investor confidence in response to the growing complexity of modern business transactions. This is not a routine committee. Its findings are expected to recommend governance and transparency improvements that could eventually translate into new disclosure requirements or amended guidance notes.

Updates to financial instrument standards: SFRS(I) 9 continues to evolve in line with its IFRS 9 counterpart. Key areas of current focus include:

- ESG-linked financial instruments and how their embedded features are classified and measured

- Hedge accounting documentation requirements for instruments tied to sustainability performance targets

- Expected credit loss model refinements, particularly for trade receivables in volatile sectors

- Classification and measurement guidance for hybrid instruments that have become common in structured finance arrangements

The ISCA taskforce findings may lead to additional transparency requirements for finance leaders, requiring more explicit communication of performance risks and assumptions embedded in financial statements. The practical implication is that companies should be reviewing their current disclosure policies now, not after the amendments are finalized.

For businesses seeking to stay ahead of these changes, reviewing the small business accounting checklist from Bizsquareaccounting is a useful starting point for structuring an annual compliance review process.

Why accounting standards deserve more than compliance-driven attention

We have worked with enough Singapore companies across different industries to say this plainly: the businesses that treat accounting standards as a compliance checkbox are the ones that get surprised. The ones that treat them as a governance instrument tend to build more durable operations.

In my experience, the most common oversight is not a deliberate shortcut. It is the assumption that last year’s approach still applies. Singapore’s accounting framework updates continuously, and a company that qualified for SFRS for Small Entities three years ago may have crossed two of the three thresholds without its directors realizing the implications. We have seen well-run companies produce financial statements that were technically compliant but structured around a framework they were no longer eligible to use.

What we find genuinely underappreciated is the relationship between clean financial reporting and capital access. Adopting SFRS(I) is a strategic advantage for companies that anticipate international investor interest, not simply an obligation for listed entities. Investors conducting due diligence on Singapore companies increasingly expect IFRS-aligned statements. Presenting SFRS(I) financials signals that a business operates to internationally recognized standards, which shortens the due diligence process and reduces perceived risk in ways that have real commercial value.

The other lesson we have learned is that proactive engagement with updates, rather than reactive scrambling at year-end, is what separates firms that file clean statements from those that file amended ones. Reading the exposure drafts from ASC, attending ISCA seminars, and subscribing to ACRA’s regulatory updates takes a few hours per year. What it prevents is far more expensive.

Accounting standards compliance is not a cost center. It is infrastructure. Treat it with the same attention you would give to any system your business depends on.

How Bizsquare helps you stay compliant

Staying current with Singapore’s accounting frameworks requires more than technical knowledge. It requires structured processes, proper documentation, and professionals who track regulatory changes as they happen.

Bizsquare provides accounting and bookkeeping services, corporate tax filing, and corporate secretarial support specifically designed to help Singapore companies meet their SFRS and ACRA obligations without the operational burden of managing it all internally. Whether a company is determining eligibility for the simplified framework, preparing for an audit, or transitioning between standards as it grows, our consultants provide the guidance and execution support needed to get it right.

The corporate tax filing guide is a strong starting point for understanding how compliant financial statements translate directly into accurate tax submissions. For companies that also need secretarial support to maintain ACRA filings, corporate secretary services from Bizsquare cover the full compliance cycle from incorporation through annual returns.

FAQ

What are the main accounting standards used in Singapore?

Singapore uses SFRS for most domestic companies, SFRS(I) for SGX-listed entities and those seeking international alignment, and SFRS for Small Entities for qualifying SMEs. All three are overseen by the Accounting Standards Council under the Accounting Standards Act 2007.

How does SFRS differ from IFRS?

SFRS closely mirrors IFRS but includes local adaptations to align with Singapore’s regulatory environment. SFRS(I), by contrast, is technically identical to IFRS in most respects, making it fully compatible with international investor expectations.

Who qualifies for SFRS for Small Entities?

A company qualifies if it meets at least two of three thresholds: annual revenue not exceeding S$10 million, gross assets not exceeding S$10 million, or total employees not exceeding 50. Eligibility is assessed each reporting period and must be documented thoroughly.

What changes are coming to Singapore’s accounting standards in 2027?

ACRA has amended SFRS(I) 1-21 and FRS 21 to address hyperinflationary currency translation, with the changes effective from January 1, 2027. Companies with exposure to hyperinflationary currencies in their reporting should begin assessing the impact now.

How do accounting standards affect corporate tax filing in Singapore?

SFRS-compliant financial statements form the direct basis for corporate tax computations submitted to IRAS. Errors or non-compliance in the financial statements create corresponding errors in tax filings, exposing companies to penalties from both ACRA and IRAS simultaneously.